Energy Markets Update

Weekly natural gas inventories

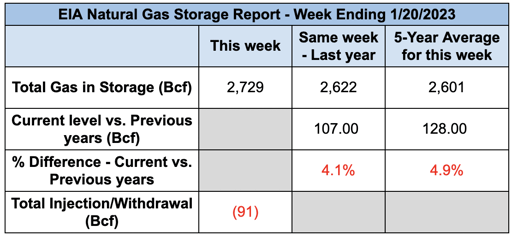

The U.S. Energy Information Administration reported last week that natural gas in storage decreased by 91 Bcf. The five-year average withdrawal for January is about 164.3 Bcf. Total U.S. natural gas in storage stood at 2,729 Bcf last week, 4.1% higher than last year and 4.9% higher than the five-year average.

US power & gas update

-

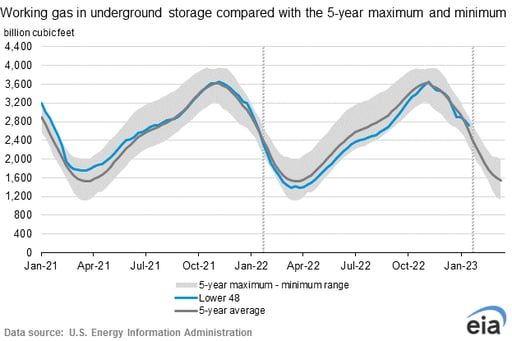

Extremely mild weather in December & January has resulted in weak demand for natural gas, putting downward pressure on markets and lifting storage inventories across the 5-year average.

-

Gas and power prices for 2023 delivery have dropped precipitously over the past month. The Feb 2023 – Dec 2023 NYMEX strip, now trading at $3.15 /MMbtu is down 45% since highs in the middle of December.

Prices for calendar year 2024 ($3.85 /MMbtu) and 2025 ($4.10 /MMbtu) have thus far been more stable, falling 18% and 10% respectively over the same period. -

Freeport LNG, the 2.1 bcf/d export terminal that has been offline since a fire in June, is expected to resume operations in mid-February under a phased-in approach.

-

European LNG import prices are also at their lowest point in over a year; a mild winter has bailed out the Germans who are currently sitting on robust storage at 84% to capacity.

-

The CEO of Chesapeake Energy, a gas and oil producer and early pacesetter in the shale revolution, has been sounding the alarm and suggesting that producers start cutting production growth plans to keep prices in check (OPEC meet OGEC?)

-

The strikingly bearish turn in markets is now leaving traders with some new information to process; how will producers react to the lower price environment after frothy prices in 2022? Will a possible recession have any impact on demand? Are we punting the risk into 2025/2026?

-

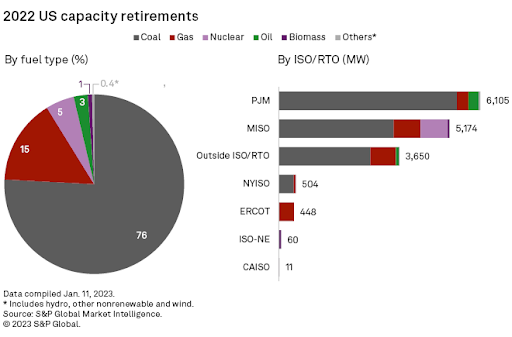

Warm weather aside, demand remains reasonably strong, led by electric power generation which has been unrelenting throughout 2022 despite higher prices. This trend will not go away—16,000 MW of capacity was permanently shuttered in 2022, and more than 75% of it was coal-fire. This means that gas must flow to keep the lights on, no matter what the price.

- We are finally expecting to see some colder weather, next week in the upper Midwest and then the following week moving to the Northeast. It’s unlikely this will shift sentiment much.

- An ongoing story however is the divergence of western markets, which continue to pay massive premiums of roughly 3-5x the average cost of gas and wholesale power compared to other regions. The West has now been bombarded with 65 straight days of gas prices > $10/MMbtu. Completion of a repair to the El Paso Gas Pipeline (2000 leg) in early February is expected to open up another 600 mcf/d and relieve the constraint.

- For further information about markets over the past year or so and how your business can mitigate this volatility and plan for the future, watch our recent webinar found here: https://www.bigmarker.com/veolia-north-america/How-to-Manage-Energy-Budgets-Through-Volatility-v2

NYS PSC Provides First Updates of the Year on ConEdison’s Delivery Rate Increase Requests for Electric, Gas, and Steam

- In February 2022 the New York State Public Service Commission (PSC) received a filing from Con Edison to increase electric delivery rates by 17.6% and gas delivery rates by 28.1%, resulting in a system-wide cost increase of $1.2 billion and $500 million respectively.

In a separate rate case filing from ConEdison in September 2022, the utility requested to increase steam delivery rates by 26% resulting in a system-wide cost increase of approximately $137 million. The revenue requirement translates to a three percent compound annual bill increase of the eight years (since 2016) which was the last time ConEdison had a steam base rate increase. - ConEdison customers should be prepared for significant rate increases from all 3 rate case filings, which are likely to impact delivery costs in the back half of this year. While the rate increases are likely to be spread out over a few years, they could also be further impacted by “make whole” payments that ConEdison has requested (see below). We are expecting the first year tranche of rate increases to exceed 5% for power and 7% for gas and steam.

- ConEdison has presented the case that the increases are needed to keep the utility’s revenues in line with the current cost obligations and add additional revenues to fund electrification and renewable energy projects required by the Climate Leadership and Community Protection Act (CLCPA) over the coming years.

- Staff from the PSC and other interested parties participated in hearing processes throughout 2022 to review ConEdison’s filing and submitted testimony to either support or oppose the utility’s proposal. The gas and power delivery rate increases were initially expected to go into effect in January 2023.

- On January 13, 2023 the PSC announced that the effective date of the newly increased rates will be suspended through April 25, 2023 as the parties continue to work on the rate settlement. ConEdison has also requested a further extension of the Suspension Date to July 24, 2023, if necessary.

- On January 12, 2023 the PSC clarified the procedural schedule for the Steam rate case which kept the Commencement of Evidentiary Hearing to May 2, 2023. ConEdision is proposing that the new rate plan take effect on November 1, 2023

- Despite the suspension of the rate proceedings for gas and power, however, ratepayers may not avoid the rate increases. ConEdison seeks to establish a “make-whole” provision covering the period January 1, 2023, through July 24, 2023, if the extension of the suspension date becomes necessary. Being “made whole” means that the utility would recover or refund any revenue under-collections or over-collections, respectively, resulting from the extended suspension period.

FERC Reviewing PJM Capacity Auction Rule Change

- In PJM’s latest capacity auction held December 2022’s, the grid operator flagged an issue that led to exceptionally high prices in the Delmarva South Power territory, which includes parts of Delaware, Maryland, and Virginia.

- This auction was intended to contract for generation capacity covering the period June 2024 through May 2025.

- Due to this price formation issue, PJM has declined to release auction results to this point citing an auction mechanics failure that resulted in high prices without any discernible reliability benefits to the region. This view was echoed my PJMs independent market monitor.

- NRG Energy, a supplier in the region that was one of the bidders, said that PJM has petitioned FERC to change the auction rules after the fact. These changes, according to NRG, would limit suppliers’ contracting and hedging options and would decrease reliability in the region.

- According to a consortium of other suppliers and advocates in both the conventional and renewable energy space, PJM’s proposal to FERC would change auction rules so bidders do not have as much information available prior to the auction and would discourage bilateral contracting and investment while raising pricing and decreasing reliability

- Many argue if FERC approved this change, it would set a precedent allowing regional operators to change auction rules after the fact if they didn’t like the results.

- PJM’s independent market monitor, Monitoring Analytics, said that if this proposal was not accepted by FERC, this region would continue to see high prices that do not reflect the supply, demand, and reliability of the region.

PJM extends delays in announcing latest power capacity auction clearing prices

- Renewables are now expected to exceed 1/4 of the U.S.’s electricity generation for the first time in 2024

- While state renewable portfolio standards have driven growth, corporate clean energy procurement has been expanding at the fasting clip, increasing ~100x over the last decade and with a record 20 GW contracted in 2022 alone

- The Inflation Reduction Act of 2022 is expected to provide another jolt to the industry.

- 2022 was not an easier year for renewables, despite positive growth. The solar industry suffered from a handful of regulatory setbacks, including a fair trade dispute that resulted in detention of solar panels by the U.S. Customs Dept., and supply chain issues that bogged down U.S. solar capacity additions throughout 2022

- Solar is back on track to increase in market share, while coal and natural gas are projected to lose ground

Corporate energy-buyers are renewing their interest in wind and solar, largely a function of reduced costs capital costs over the past decade (47% and 71% respectively) - Increased utility rates and tax credits from the Inflation Reduction Act (which in some cases can reach 50%), have further incentivized a solar industry bounce-back in 2023

- Solar companies in particular have seen tremendous growth following passage of the IRA in July 2022 – industry leader First Solar, Inc., for instance, experienced a 69% spike in shares in the following months

- In 2022, Shell PLC was the leading corporate buyer for renewables, contracting over 1.2 GW of clean energy. Texas, which uses solar panels to power its oil rigs, was the leading state in clean energy procurement with a capacity of 27 GW.

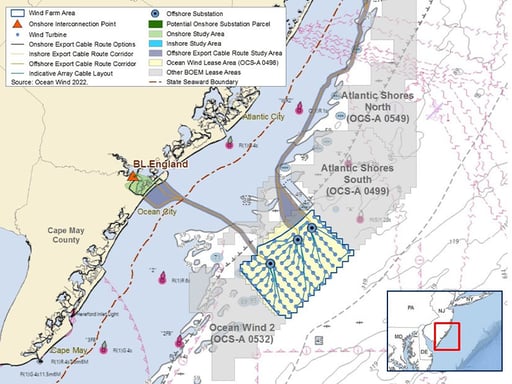

East Coast Wind Energy Developments

- The New Jersey Board of Public Utilities (NJBPU) recently approved nearly $1.1 billion in transmission system upgrades to the state’s electricity grid.

- These upgrades will enable electricity generated from offshore wind assets to be connected to the power grid and are a part of the state’s plan of creating 7,500 MWs of offshore wind capacity by 2035.

- The project, the Larrabee Tri-Collector Solution (LTCS), is estimated to cost $504 million and was proposed by JCP&L and Mid-Atlantic Offshore Development, a joint venture of EDF Renewables North America and Shell New Energies US.

- The NJBPU also awarded additional onshore transmission upgrades to accommodate the additional generating capacity from LTCS and other planned offshore wind projects.

Source: BOEM

- These awards went to ACE, BGE, LS Power, PECO, PPL, PSE&G, and Transource at an estimated cost of $568 million.

- Ørsted and PSEG are the owners and developers of the Ocean Wind project, which will be New Jersey’s first utility-scale offshore wind farm. Project construction is scheduled to begin in early 2023, with commercial operations expected at the end of 2024. A second and adjacent project, Ocean Winds Two, is expected to add an additional 1,100 MWs of generating capacity. Construction on that project is not expected until 2028.

Natural Gas Storage Data

Market Data

Use the filters to sort by region

Market data disclaimer: Data provided in the "Market Data" section is for the newsletter recipient only, and should not be shared with outside parties.