Energy Markets Update

Weekly natural gas inventories

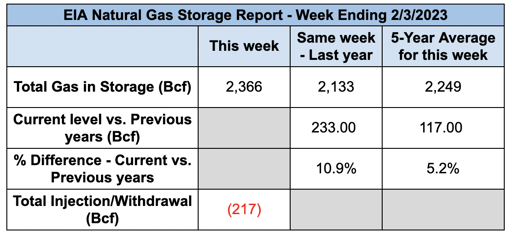

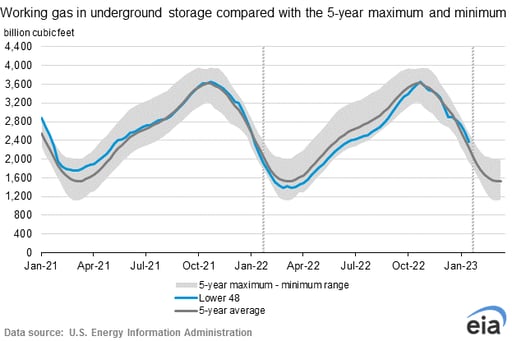

The U.S. Energy Information Administration reported last week that natural gas in storage decreased by 217 Bcf. The five-year average withdrawal for February is about 162 Bcf. Total U.S. natural gas in storage stood at 2,366 Bcf last week, 10.9% higher than last year and 5.2% higher than the five-year average.

US power & gas update

-

Power and gas markets continued their rout over the past two weeks, but the heaviest losses have been contained to the 2023 calendar strip.

-

The balance of 2023 NYMEX gas contract has been testing the $3.00 support level this week, down 15-20% over the past 2 weeks and 45% over the past 2 months. The 2024 and 2025 strips, trading at $3.70 and $3.90 respectively, have demonstrated more resistance but have each shed about 7% over the past 2 weeks.

-

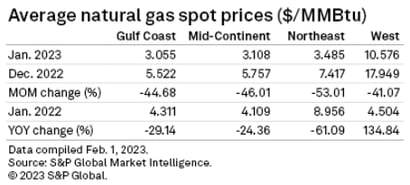

Spot prices have also been getting crushed month over month.

-

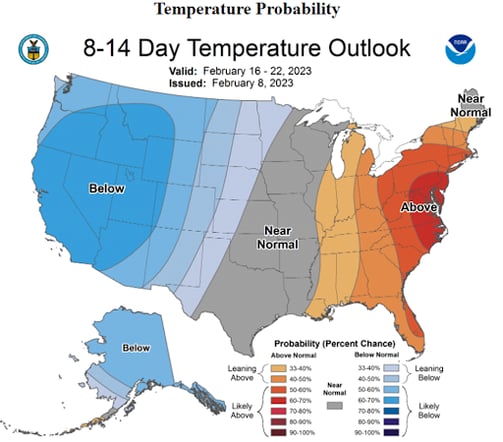

Large swaths of the Central US and East shivered through a 2-day cold snap on Feb 3 and 4. We witnessed some seasonal high water marks for spot market gas and power, but it was short lived. Prices quickly normalized with the thaw over the weekend.

-

Looking forward, temperatures are expected to be mild for the coming weeks in the major eastern load centers. This is starting to look like the beginning of the end for the winter bulls.

Source: NOAA

Source: NOAA -

The price of coal deliveries for Q2 & Q3 of 2023 have also dropped by as much as 50% YOY, which may keep a lid on spark spreads later this year, however the Energy Information Administration is still calling for a significant decline in 2023 coal-fired production. EIA forecasts that coal will make up 18% of generation in 2023 and 17% in 2024, as compared to 20% in 2022.

-

Freeport LNG, the 2 Bcf/d export terminal that has been shuttered since a fire in June 2022, has been approved to start ramping up in mid to late February, however consensus is that it will not reach full capacity until mid-March.

-

West coast markets were again the outlier in January, with gas settling at about a $15/MMBtu premium to NYMEX. Earlier this week, Governor Newson requested that FERC launch an investigation into surging gas prices that have propped up gas and power markets to unsustainable levels since November. He is right to do so—the event has shed an ugly light on price formation in the natural gas market. There was also an En Banc session in California this week to dive into the issue.

PJM prepares to issue massive non-performance penalties

-

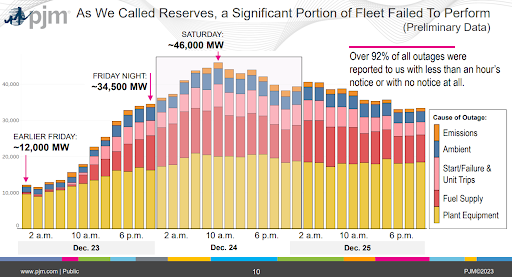

PJM is preparing to dole out a historic $2B in penalties to unreliable generators following large-scale generation outages and power plant failures in late December.

-

Record cold temps beginning Dec. 23 – with some PJM territories’ temps dropping 29 degrees in less than a day – caused unexpectedly high demand up to 40,000 MW greater than the 10-year average.

-

PJM had a peak load of 134,765 MW on Dec. 23, 2022. However, generation outages reached ~23% of PJM's total capacity (46,000 MW) by Dec. 24.

-

Anticipating 29 GW of available reserve capacity based on generator availability data, PJM was shocked when ~6,000 MW of generation called online was unavailable.

-

In 2016 PJM implemented its Capacity Performance program, which makes generators liable for massive penalties if they do not provide power when called upon in scarcity situations. They are of course compensated for their availability; Capacity Performance is the stick to go along with the carrot. However, since its inception, there have only been a couple of very regional Capacity Performance events. This is really the first widespread event since its inception and clearly generators had grown complacent.

-

There is a similar program in New England, and it too had non-performance issues over the same period, however they were less severe and aggregate penalties were approximately $39 million.

NC customers can now supplement their power with 100% renewables

-

Duke Energy, a North Carolina utility, is expanding its electricity offerings to allow customers to voluntarily purchase 100% renewable energy.

-

Duke’s Green Source Advantage Choice program will be expanded to 4,000 MW of capacity, increasing the size of the program tenfold.

-

If approved, the program will resource renewable energy from previously contracted solar agreements, but it may also contract for additional wind capacity as well.

-

Customers in this service territory will now have options to green-up their power supply without having to enter into virtual power purchase agreements.

-

The program may take 10 years to reach the targeted capacity to give Duke time to procure the necessary resources.

-

The program comes on the heels of 2021 North Carolina energy legislation that required a similar program for all utility customers. This legislation, which will line up with Duke’s plans to procure renewables, requires 45% of solar generation come from power purchase agreements and 55% come from utility owned projects.

-

Duke has additionally proposed a Clean Energy Impact program which would allow customers to claim a certain percentage of their electricity purchases as renewable for sustainability goals.

Minnesota Accelerates Target To Achieve Carbon Free Energy

Will this become a model for other MISO Members?

-

The Minnesota Senate passed a bill on Feb 7th to accelerate the timeline for the state’s utilities to shift to carbon-free electricity generation forward by 10 years to 2040. The state’s Democratic governor, Tim Walz signed the bill into law the same day.

-

The bill marks the first advancement to Minnesota’s climate goals since 2007. At that time, the Generation Energy Act of 2007 set the target for an 80% reduction by 2050.

-

Sceptics have voiced concern about the ambitiousness of accelerating mandates, noting that statewide emissions have only decreased by 8% since 2005. Other opponents in the legislature expressed concerns about reliability and cost increases that will be incurred as utilities will now have a shorter transition time to address other hurdles that come with adding wind and solar capacity. Republicans also warned that other energy-producing states in the Midcontinent Independent System zone (MISO) could file lawsuits to try and block the law just as North Dakota did in 2007.

-

MISO publishes an annual Regional Resource Assessment (RRA) report which aggregates publicly announced plans and goals and uses them to develop an indicative view of how the mix of resources across the MISO region might change over time. The RRA’s published map below will need to be updated after the bill is signed into law.

Source: MISO 2021 RRA Report

-

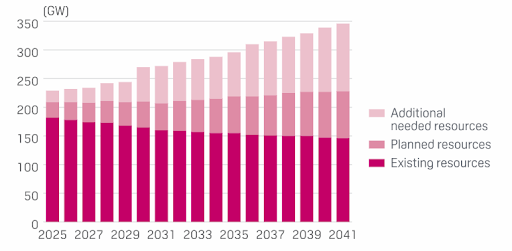

According to the 2022 RRA report, MISO members indicated they are expecting that the increase in capacity will be primarily from a mix of wind and solar, both of which have lower accredited capacity values than thermal resources like coal and natural gas. The chart below illustrates the point that more than 100 GW of new capacity will likely be needed by 2030, and 200 GW may be needed by 2041 to align with capacity demand.

Source: 2022 MISO RRA Report

-

Adding another wrinkle in Minnesota's 100% target is that even by MISO’s own findings, renewable energy integration will get significantly more complicated when penetration reaches 30%-40%. “Oh ya betcha” that Minnesota’s largest energy provider, Xcel Energy, and others now have 17 years to achieve the new mandate.

Allete, Grid United partner on $2.5B proposal to link US East, West grids

-

Grid United and Allete announce plans to develop a $2.5 billion, 385-mile high-voltage transmission line (the “North Plains Connector”), which will mark the nation's first transmission connection to flow between three regional electricity markets (SW Power pool, Midcontinent ISO, and Western Interconnection).

-

The transmission line will create 3,000 MW of transfer capability, which will be key as national electricity demand continues to ramp up.

-

Connecting Montana and North Dakota’s grids will mitigate impacts of extreme weather occurrences, accommodate growing electricity demand and boost overall grid reliability.

-

Allete is undergoing transmission investments as part of the company's ‘Sustainability-in-Action’ campaign. Large high voltage transmission lines will be critical to the success of clean energy transition, particularly due to the cost competitiveness of locating large renewable energy generation corridors in the middle of the country.

-

Project permitting to begin in 2023, line will become operational in 2029.

Source: North Plains Connector

ISO-NE Capacity auction to resume downward trend

-

In 2023, the New England independent system operator plans to focus on "advancing a reliable clean-energy transition through innovation and collaboration," according to the grid operator's 2023 Annual Work Plan.

-

Rhode Island, Connecticut and Massachusetts have specific requirements for offshore wind while the soaring natural gas prices and relatively low prices to build onshore wind and solar drive more renewables.

-

On a related note hover, on January 19, Avangrid filed a Petition for Appeal with the the Supreme Judicial Court (SJC), seeking to get out of the offshore wind project it signed with Massachusetts in April 2022. It has cited its inability to finance the project due to changes in economic circumstances.

-

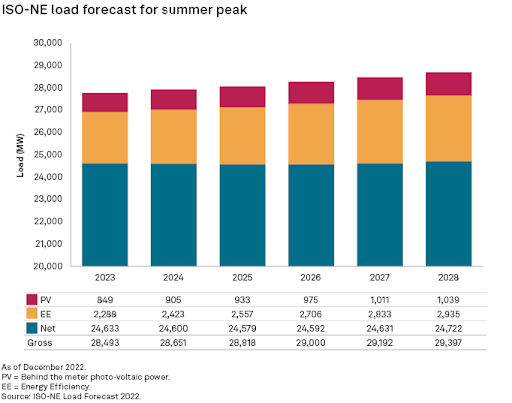

The Inflation Reduction Act tax credits make renewables even more appealing, hence ISO-NE’s forecast that 50% of the 2028 total peak summer generation will come from renewables — an increase of 1.8 TWh from the second-quarter 2022 power forecast.

-

All these factors result in a forecast indicating that new renewables are more economical than fossil fuel plants under the current market and incentive environment.

-

S&P forecast 4.3 GW of fossil fuels plant retirements during the 2025-2028 period, in addition to the 1,700 MW gas-fired Mystic River 8 and 9.

-

The ISOE-NE 2022 load forecasts included an increase in behind-the-meter solar of about of 4.1% annually, savings from energy efficiency by an average of 5.1%, and essentially no net load growth (fig. 1).

-

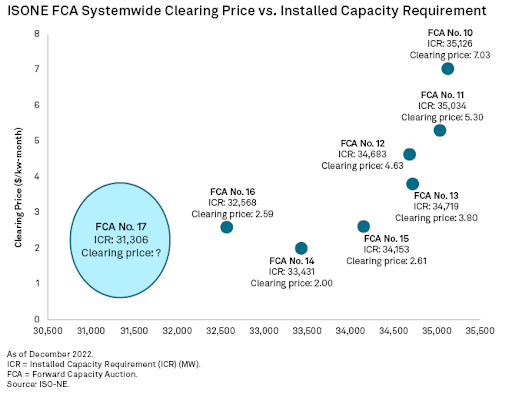

The combination of low load growth, increasing renewable capacity and few retirements create downward pressure on capacity prices in ISO-NE. These conditions prolong the recent trend, where the last four FCAs have cleared at less than $4 per kW-month.

-

For the upcoming FCA 17, the installed capacity requirement is set to 31,306 MW, more than 1,200 MW less than the installed capacity requirement for FCA 16, which cleared at $2.591/kW-month systemwide, and more than 2,800 MW less than the installed capacity requirement for FCA 15, which cleared at $2.611/kW-month systemwide.

-

While many other factors influence bids, recent clearing prices plotted with installed capacity requirements for each FCA show a decrease in clearing price as the installed capacity requirement decreases. FCA 17 has a lower installed capacity requirement than the previous six auctions, which increases the risk of a historically low clearing price for this auction. For this reason, Market Intelligence Power Forecast projects a clearing price comparable to FCA 14, $2.001/kW-month.

Natural Gas Storage Data

Market Data

Use the filters to sort by region

Market data disclaimer: Data provided in the "Market Data" section is for the newsletter recipient only, and should not be shared with outside parties.