Energy Markets Update

Weekly natural gas inventories

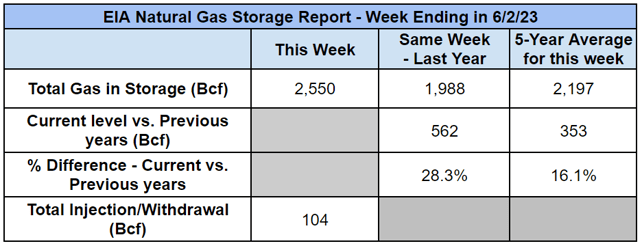

The U.S. Energy Information Administration reported last week that natural gas in storage increased by 104 Bcf. The five-year average injection for June is about 82.8 Bcf. Total U.S. natural gas in storage stood at 2,550 Bcf last week, 28.3% higher than last year and 16.1% higher than the five-year average.

US power & gas update

- Gas and power prices have declined slightly over the past 2 weeks, setting new lows for the balance of 2023 and finally putting pressure on outer years. Bearish fundamentals are now weighing more on the 2024-2026 strips, which are down 3-4% over the past two weeks and all below $4.00 per MMBtu.

- The national gas storage surplus now sits about 16% above the 5-year average and 30% above last year.

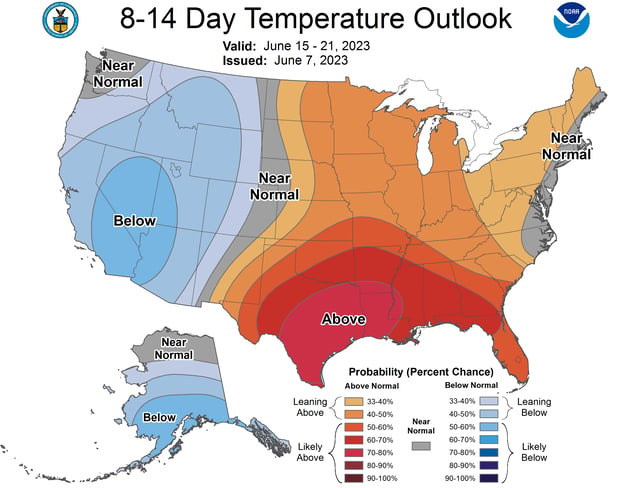

- Cooler spring temperatures have taken hold in much of the Northeast, pushing down res/com demand and likely maintaining the current storage surplus well into June. Future weather forecasts show above-average summer temperatures being brought by El Niño – though it’s certainly not being felt yet.

Source: NOAA

- The healthy storage surplus position has not changed significantly since March but reflects a delicate counterbalance between moderate weather and a robust demand from the power sector. Gas demand from the power sector is up 10% year-over-year and regularly setting new monthly records.

- We suspect the surplus will give way rather quickly if summer temperatures are realized around prior year averages. This could be a near term buy signal, i.e., “buy the rumor, sell the news,” particularly in lieu of falling gas rig counts that have been previously reported on.

- With June marking the beginning of summer “demand tag” season, enrolled customers may be seeing initial messages from the Veolia team this week. Preliminary forecasts from both New England and New York ISO indicate that there are sufficient resources to meet summer demand, although heat waves could still result in emergency protocols in New England.

- NYISO anticipates a peak demand of 31,765 but states that it has no reliability concerns until loads surpass 35,400 MW. However, a reliability assessment last year identified margins as little as 50 MW in 2025 due to anticipated peaker plant retirements, and this week NYISO sounded the alarm that stakeholders will need to allow for better coordination between retirements and new generation additions over the next decade.

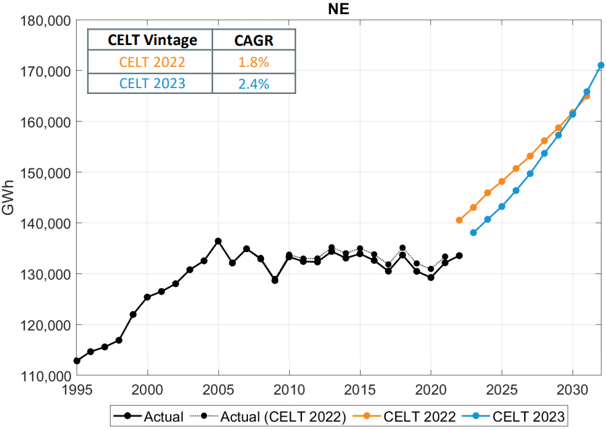

- Up from last year, New England ISO forecasts a peak demand of 24,605 MW this summer which could reach 26,421 during a prolonged heatwave. Incremental increases in peak summer load are projected for years to come as regional systems rush to adopt heat pumps and other electrification measures.

ISO-NE Annual Gross Energy Forecast

Source: ISO-NE

Source: ISO-NE

- This week the California Energy Commission approved a new load shift goal—7000 MW by 2023—which includes demand response programs and time-of-use rates that incentivize shifting or curtailment of electricity use away from the early evening constraint periods.

- In other news;

- CT Rate Case: Connecticut has approved a rate decoupling model for electricity, which may spur additional energy efficiency investment by utilities.

- Last week the nation avoided the risk of economic calamity associated with defaulting on its debt and the FED will make a call on whether to pause or resume interest rate hikes on June 14th.

- Parts of the Northeast are experiencing the worst air quality ever recorded due to Canadian wildfires.

Energy concessions included in US debt ceiling deal

- The country narrowly avoided the economic calamity of a national default last week with President Biden signing a bipartisan debt ceiling agreement. There were a few energy-related topics that made their way into the deal.

- The bill streamlines permitting and siting processes for energy infrastructure projects by amending the National Environmental Policy Act (NEPA) of 1970, under which the process of obtaining permitting for energy infrastructure projects has become quite the headache–previous reviews indicated that the page length of the average environmental impact statement exceeds 600 pages and takes 5 years to complete.

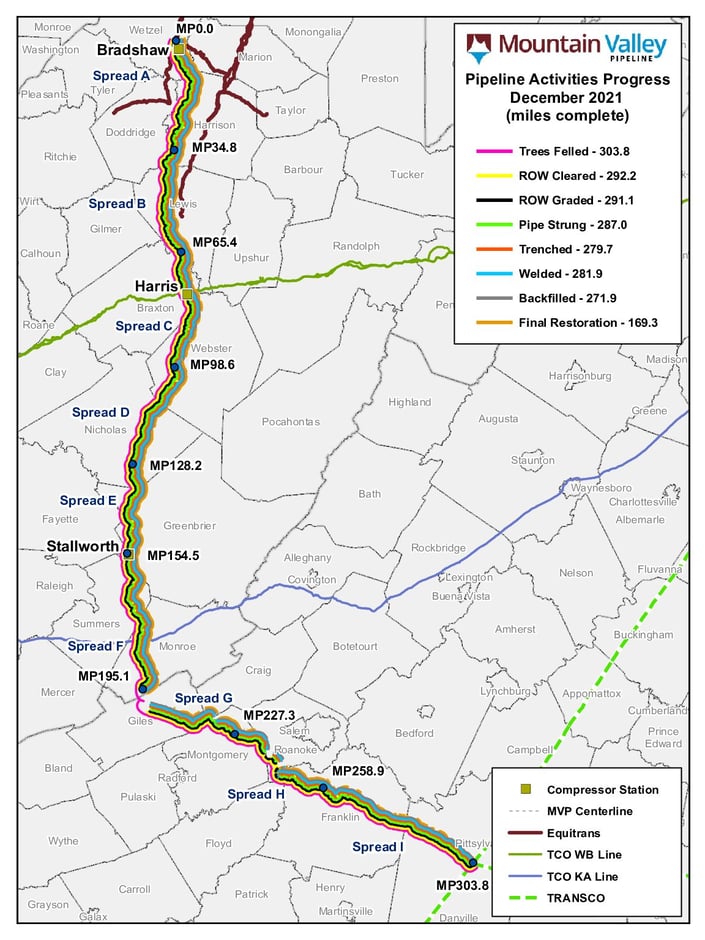

- Notably the $6.6 billion Mountain Valley natural gas pipeline, which has been stalled by legal challenges to the project’s permitting for years, is now authorized for completion (much to environmentalists’ dismay but the project was already 95% complete and provides benefits to ratepayers, so just finish the damn thing already, right?!?)

MVP has been mostly complete since 2021

Source: Mountain Valley Pipeline Info

- MVP is a 303-mile project that will bring cheap shale gas from northwestern West Virginia to southern Virginia and support the Mid- and South Atlantic.

- Under this legislation all permitting approvals for the MVP will be issued no later than June 24th, 2023.

- The bill also protects this pipeline from further legal battle by transferring jurisdiction to review such proposals to the D.C. circuit.

- In an earlier, more radical version of the bill, House Republicans sought to roll back tax credits for emissions-free energy projects established in the Inflation Reduction Act of 2022. Biden’s bill excluded this provision from his final bill, leaving the IRA unchanged for now.

- The bill is arguably a mini-win for fossil fuel industry advocates like House Speaker Kevin McCarthy. So what does the future for energy infrastructure look like? In exchange for Biden’s signature, McCarthy has pledged to endorse Democrats’ ambitious clean energy targets going forward.

- Though the likelihood of Republican support for energy transition seems slim, permitting reform will remain an interesting point of debate going forward as Democrats and Republicans both seek their own definitions of “energy independence.”

Texas leads growth in renewable energy and batteries

- In the past few decades Texas has emerged as the U.S. hub for renewable energy development. Just last year the state installed 7350 MW of new wind and solar projects, significantly outpacing California’s 2700 MW.

- Texas has some notable advantages: legendary wind speeds, cheap labor, abundance of land, and lax regulations.

- Today a significant share of energy business is being redirected from big oil and gas in favor of solar, wind, and a nuclear fleet, which all together, are responsible for 40% of Texas’s electricity mix.

- The “zero-emissions trio” has nearly caught up to natural gas, which contributes up to 40% of the state’s generation as well.

Source: ERCOT

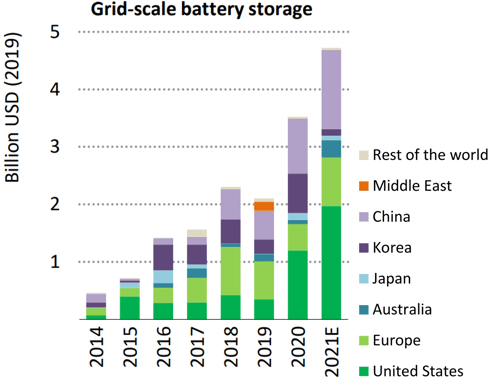

- With wind and solar on the rise, investment into utility-scale battery energy storage systems (BESS) has followed suit. In March, Texas became home to the world’s largest standalone battery storage facility (at 500 MWh). Overall the state accounts for 31% of new U.S. grid-scale energy storage and is expected to contribute an additional ~30MW by the end of this decade. Nationwide, installed generating capacity of battery storage is expected to surge 10x by 2050.

- Many critics of wind and solar cite power production variability – i.e. the inability to produce consistent energy flow across all climates, seasons, etc. – as their main shortfall.

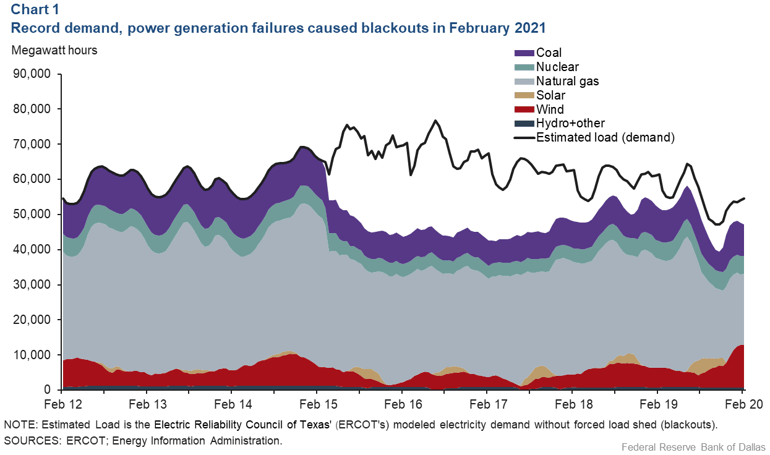

- In Texas, where grid reliability has been tested by weather emergencies pushing the grid to the brink of collapse (winter storm Uri, here’s lookin’ at you), the need for reliable power generation is more apparent than ever.

Sources: ERCOT, EIA

- Even so, energy remains an intensely politicized topic and renewables and BESS still face obstacles at the legislative level. Just this week Texas lawmakers approved subsidies for fossil fuel plant construction that may shift focus away from renewables.

- Globally, energy storage markets will continue to be dominated by China and the U.S.

Investments in Grid-Scale Battery Storage By Country 2021

Source: IEA

Source: IEA

Summer of RNG uncertainty: birth and death by regulation

- The RNG sector was a leading beneficiary of the investment in decarbonization plays throughout 2022, and 2023 might double down on that growth.

- Within the $370 billion green energy allocation included in the IRA last year, was an investment tax credit that would reimburse 40% of a qualified biogas project's development costs, as well as a renewed $0.50/gal fuel tax credit for RNG used as a transportation fuel.

- These are massive tax incentives for notoriously capital intensive projects and they have set off a race to identify, finance, and construct new projects before the credits expire in two years.

- The IRA program aimed to support the development of RNG projects by providing financial assistance and guidance to potential investors. As a result of this program, the RNG industry experienced a surge in investment activity during summer 2021 and 2022.

Source: S&P

- RNG industry numbers cite nearly 300 projects in planning on top of 180 projects under construction. That would create an industry more than three times larger than today’s sector, in which 281 projects currently produce fuel largely destined for transport use. Nevertheless, US fossil gas production is about 90 billion cubic feet per day, so the additional production of roughly 300 billion cubic feet per year currently planned or in construction would barely dent the total US gas profile. At most, RNG could displace around 16 percent of current fossil gas consumption, according to industry-supported research. Other studies suggest the share is much smaller.

- Additional regulatory equivocation adds uncertainty to the market, but so far has not ended the party. Most notably, a newly proposed pathway to monetize RNG by contracting with electric vehicle manufactures threatens (i.e., the “eRIN” program) appears to be getting scrapped by the US EPA in its ongoing rulemaking process (see e.g., recent report by Reuters). In a 700-page RFS proposal published in December, the EPA quietly proposed the creation of eRINs, where EV manufacturers - Ford, General Motors, Tesla, etc. - would be allowed to generate RINs from sales of their vehicles. This would illegally transform the RFS into a new Biden administration subsidy for EVs at the expense of US-produced biofuels such as ethanol, biodiesel and renewable diesel, whose growth was the main reason for creating the RFS. This provision would force small refineries serving remote areas of the country to send checks directly to companies like Elon Musk and Tesla, and every gallon of gasoline and diesel fuel made in the U.S. would cost even more to produce due to an eRIN-inflated RFS.

Also, a Federal Energy Regulatory Commission (FERC) technical conference this week prompted by a filing from a pair of fossil gas midstream giants could prompt rule changes that significantly hamper the RNG buildout by imposing new technical standards and separate tariff processes on the sector. FERC accepted the Florida Gas tariff proposal but suspended the effective date to Aug. 27 subject to the outcome of the technical conference, as well as an administrative law judge hearing that was held in abeyance. - All told, these developments threaten to remove a new and budding RNG pathway (power generation) while casting additional doubts over the existing pathway (pipeline injection).

- In recent years, major banks have found that the RNG sector matches their business model in ways that expanded opportunities in renewable electricity have not. The blend of low-risk bond-issuing municipal counterparties, public company transaction types and familiar gas-based market and pricing structures have drawn large oil and gas firms like BP and Marathon Petroleum into the US RNG industry.

- Barclays and Guggenheim, in March 2023, represented Marathon Petroleum and private equity firm Cresta Capital in Marathon’s $100 million purchase of a 49.9% share of RNG firm LF Biofuel, one of a slate of recent bank-facilitated deals. Private equity-backed RNG producer Amp Americas ended 2022 inviting bids from oil company buyers on a $1 billion valuation alongside Starwood Capital-owned BerQ RNG, all tempted into the market by BP’s banner $4.1 billion to buy RNG producer Archaea Energy on the advice of Morgan Stanley.

Source: S&P

Natural Gas Storage Data

Market Data

Market data disclaimer: Data provided in the "Market Data" section is for the newsletter recipient only, and should not be shared with outside parties.