Energy Markets Update

Weekly natural gas inventories

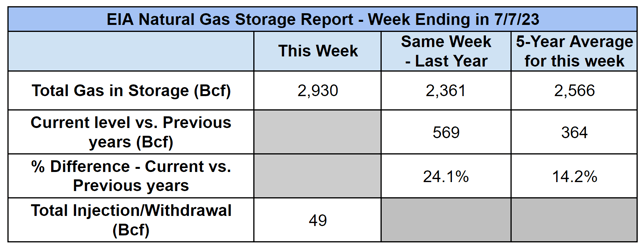

The U.S. Energy Information Administration reported last week that natural gas in storage increased by 49 Bcf. The five-year average injection for July is about 42 Bcf. Total U.S. natural gas in storage stood at 2,930 Bcf last week, 24.1% higher than last year and 14.2% higher than the five-year average.

US power & gas update

- Sweltering summer heat, high cooling demand and flattened production have recently placed some upward pressure on gas and power markets. NYMEX spot prices are up 17% from prompt month pricing and futures gained momentum at the start of July as well.

- Yet the market lingers in contango – where prices for ‘24-’26 remain more expensive than the current year. Gas bulls continue to grapple with the million dollar question: when will spot prices rebound?

- The South-central US regional market has tightened slightly due to higher-than-expected cooling demand via (yes, another) prolonged heatwave in Texas.

Source: S&P

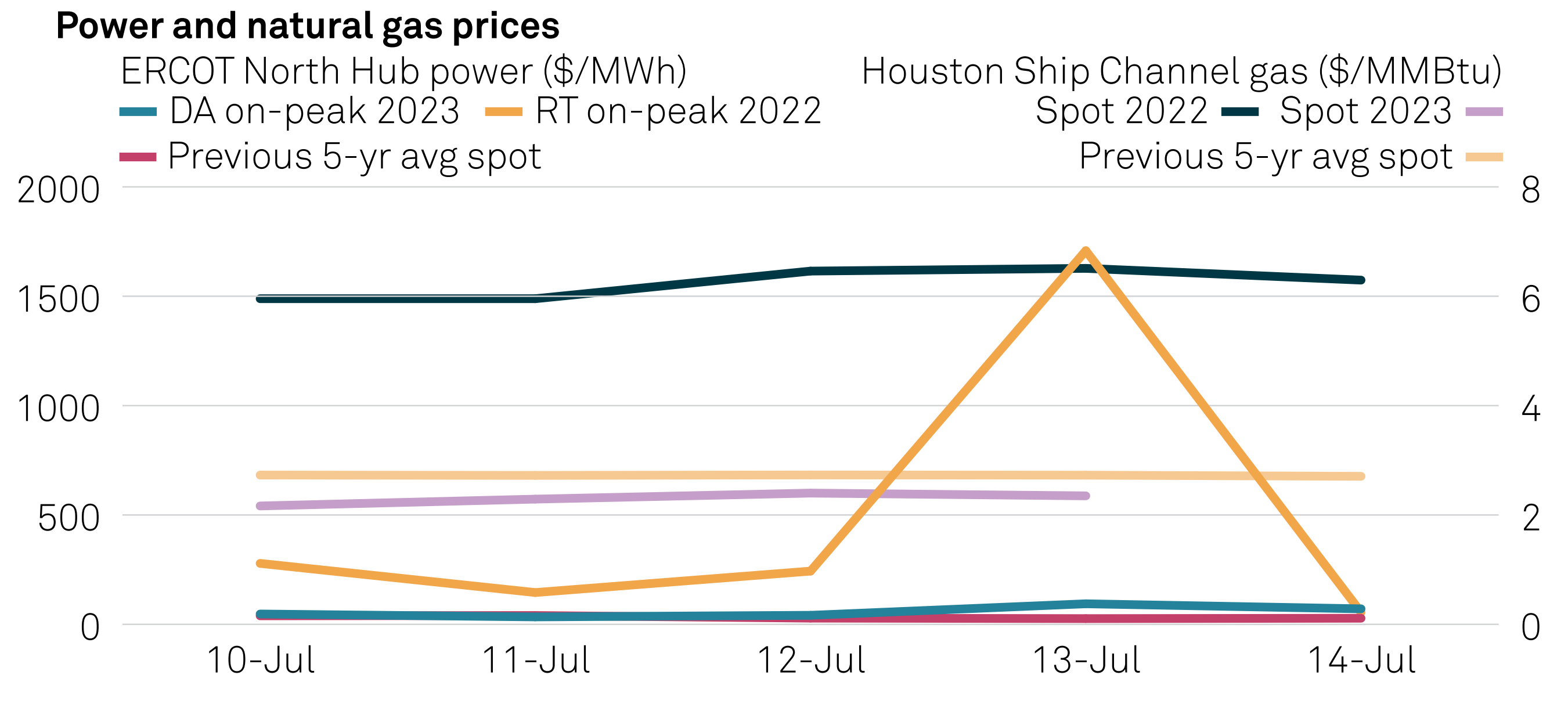

- Power prices climbed to 21% higher than the five-year average, though remain relatively tame. During a similar 5-day scorcher in 2022, regional power prices soared to $1,708/MWh. Last week, the market largely shrugged off these conditions and prices remained under $50/MWh.

Source: S&P

- Cheap gas and strong renewable power generation from solar and wind are responsible for keeping the grid afloat and electricity prices down amid fossil fuel plant outages. As a share of total power, renewables met 40% of peak demand last Wednesday reaching a record 31 GW.

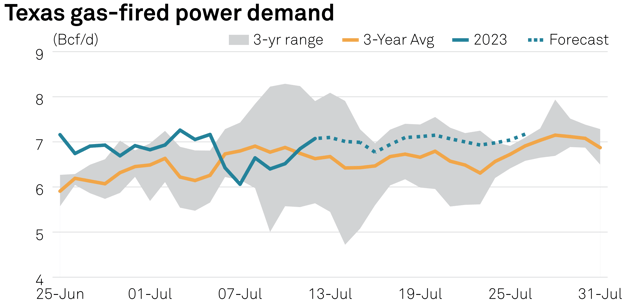

- The ERCOT grid has proven resilient (thanks to renewables) in the face of weeks-long triple digit temperatures. This is encouraging since record demand is projected to be broken another four times in the next two weeks.

- Outside the Lone Star State, the rest of the country has emerged from a cool June and many can expect above average temperatures in coming weeks. The Northeast, however, will remain temperate.

- With hotter temperatures and peak cooling season still on the horizon for everyone (late July through August), gas-fired power demand will be the key driver of gas prices later this summer.

- With hotter temperatures and peak cooling season still on the horizon for everyone (late July through August), gas-fired power demand will be the key driver of gas prices later this summer.

Source: NOAA

- Algonquin Citygate (the pricing hub for Boston-area consumers) saw some volatility after the July 4th weekend, with prices spiking from $1.99/MMBtu to $7.93/MMBtu overnight. Planned outages along the Algonquin Gas Transmission (AGT), which had been restricting natural gas flows into NE since June, were resolved late last week and the price volatility has since calmed.

- Storage inventories have continued maintaining their surplus this summer injection season. Gas in storage last week was 24.1% higher than last year and 14.2% higher than the 5 year average.

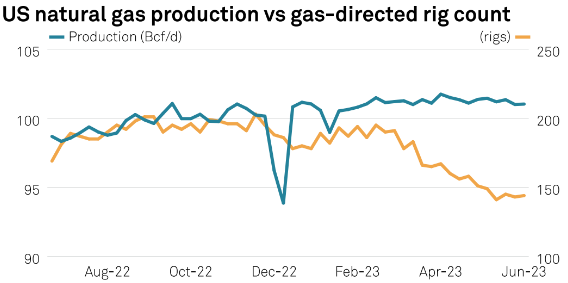

- By mid-June, the US natural gas rig count (an early indicator of future output) had declined 21% from the start of this year, primarily driven by a reduction in output as producers’ hopes of a natural gas price rebound sank. However, last week 11 rigs came back online, leaving analysts scratching their heads.

- Prior to this, the declining rig count supported bullish sentiment for 2024 gas & power prices. We'll have to wait and see if last week's uptick was fluke, or a genuine shift away from the trend we've witnessed so far this year.

Source: S&P

Source: S&P - Prior to this, the declining rig count supported bullish sentiment for 2024 gas & power prices. We'll have to wait and see if last week's uptick was fluke, or a genuine shift away from the trend we've witnessed so far this year.

- This week Rio Grande LNG – a subsidiary of NextDecade – finalized a landmark $18.4B investment in phase 1 of the U.S.’s largest-ever LNG export facility in Southern Texas, which at full capacity can produce 27M tonnes of LNG.

- Notably, the facility features a carbon capture component that can store 5M tonnes of CO2 emissions per year, lowering emissions up to 90%!

- A few weeks ago we reported on energy concessions included in Biden’s debt ceiling plan; notably, the bill finally authorized completion of the Mountain Valley natural gas pipeline (spanning 303 miles and $6.6B) which has been tied up in a legal battle for years.

- But hold your horses – this week, construction has been stalled yet again by legal debate over the Endangered Species Act. Mountain Valley is now considering an emergency appeal to the Supreme Court to continue operations. Construction is 95% done...so we hope they just finish the pipeline, damnit!

- The Illinois Commerce Commission (ICC) is seeing an unprecedented number of rate cases this year. Two of the state’s largest electric providers and four gas utilities are lobbying for increased rates – worth a whopping $2.8B and $800M respectively.

- Electric providers Ameren and Commonwealth Edison insist that such increases are necessary to address inflation and clean energy demands made under the landmark 2021 Climate and Equitable Jobs Act, which requires electric companies to partake in a “multi-year integrated grid plan.”

- If approved, customers could pay upwards of $140 more/year for gas alone. Some 12.3% of customers of these utilities currently undergoing rate cases are already behind on bill payments, so the hikes do not bode well.

- SoCalGas, Georgia Power Co, and ConEdison are in the midst of similar tussles, proposing hefty rate increases in the face of expensive clean energy targets.

Carbon accounting 101: everything your business needs to know

- The touted “road to net zero” is at the forefront of many businesses’ minds as ambitious ESG targets and murmurs of corporate sustainability have taken industry by storm.

- Carbon accounting empowers businesses to quantify their direct and indirect contribution to global fossil fuel emissions. Utilizing the results to set tangible emissions reduction targets will be essential for curbing climate change.

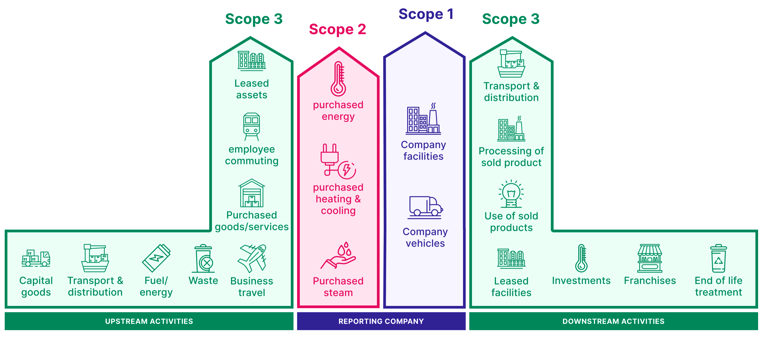

- The Greenhouse Gas Protocol is currently the most preferred and widely-adopted standard for emissions accounting. The protocol breaks emissions into 3 categories:

- Scope 1, covering direct emissions from sources owned or controlled by a company – for instance CO2 emitted during the manufacturing of a computer.

- Scope 2, highlighting the emissions associated with purchased electricity. Emissions occur at the location they’re generated at (i.e. a power plant), but are accounted for at whichever facility the electricity is consumed (i.e. a manufacturer that bought and consumed said electricity from the plant).

- Scope 3, capturing granular “upstream” and “downstream” emissions. Simply put, these are emissions that a company is not responsible for via direct production activities or from assets controlled by them; rather how their activity contributes to emissions across the corporate value chain. For instance, if a consumer purchases a product made by company A, scope 3 reporting would account for the emissions caused by that end consumer’s car trip to buy the product. Scope 3 makes up roughly 80% of a business’s true GHG emissions.

The GHG Protocol, by scope:

Source: Circularise

Source: Circularise

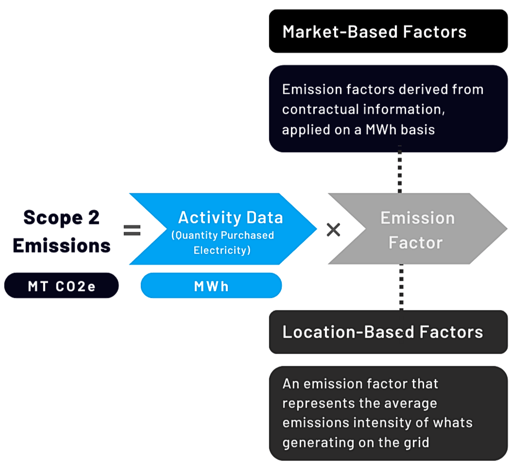

- So, what does the math look like? We use emissions factors to translate such business activities – like office energy consumption or vehicle fuel combustion – into a standard emission (CO2e). Emissions factors correlate the rate at which an activity is performed to their relative GHG emission potential. Emissions factors are the “secret sauce” of carbon accounting as they standardize the correlation between everyday business activities and their emissions.

- Selecting the appropriate emissions factor coefficient can be difficult as there are so many kinds; some are based on fuel type and geographic location, while others consider the nitty gritty of individual contracts and supplier-specific emissions.

- The emissions factor used also depends on whether a company is utilizing market-based or location-based accounting (the GHG protocol encourages both).

- Location-based accounting uses emissions factors specific to the region or grid associated with electricity consumption, while market-based accounting is based on purchased electricity. Businesses are able to claim benefits from contractual arrangements under this method –i.e. REC’s, PPA’s, and other energy attribute certificates.

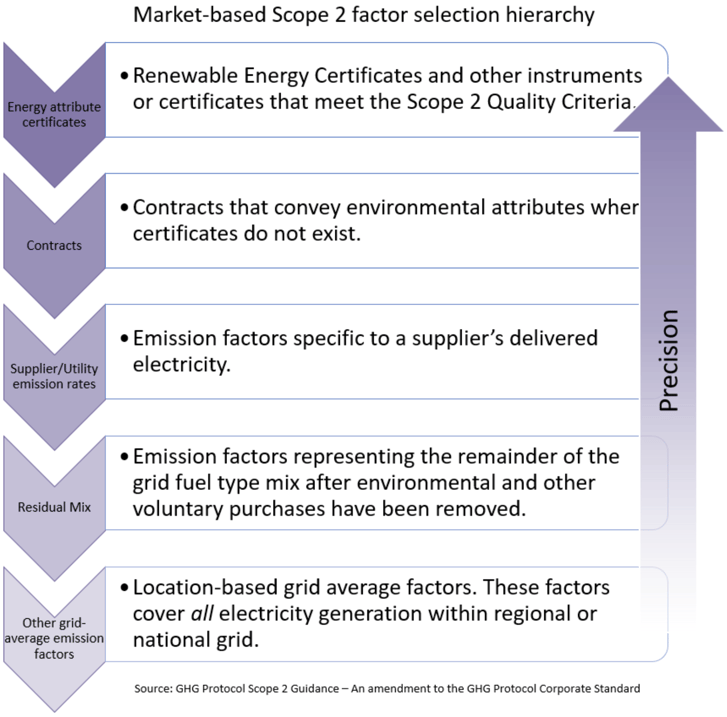

Market vs. location-based factors under scope 2

Source: Watchwire

- The GHG Protocol has established a hierarchy for selecting market-based emissions factors; thus while it’s left up to companies’ what coefficient they use, it’s recommended to use factors as specific (and thus accurate) as possible. Ideally, the order of selection travels down the food chain – i.e. the “residual mix” factor should only be used to calculate leftover emissions after energy attribute certificates, contracts, and so on are accounted for.

Source: GHG Protocol

- While carbon accounting is undoubtedly complex, the extra time and effort is worthwhile as identifying where Scope 1, 2, and 3 emissions originate from provides businesses the knowledge needed to reduce their impact at the source.

- Ultimately, these conversations are being heard in lunchrooms and boardrooms more and more. Having a plan for how to calculate these emissions - and more importantly how to lessen your contribution long term - will be a key component of corporate responsibility going forward.

DoE awards 7 vouchers under GAIN initiative

- The topic of nuclear power has become an increasingly polarizing one. While some embrace the controversial technology, applauding its small carbon footprint and long term reliability, others fear the risks associated with a potential plant meltdown or failure – cue Chernobyl nightmare sequence.

- As Russia just recently acquired Europe's largest nuclear power plant and a new nuclear facility in Georgia has begun operations, these debates are hitting the spotlight once more.

- In Europe the divide is abundantly clear between Germany and France; where the former has recently decided to decommission all its nuclear plants and the latter is a worldwide nuclear frontrunner.

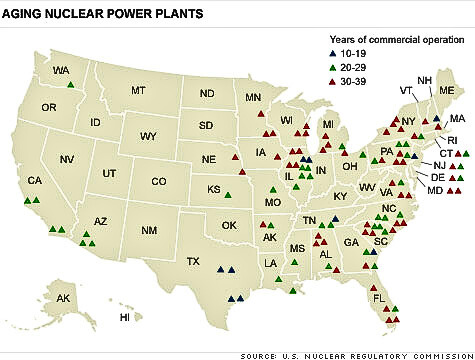

- Nuclear accounts for 18% of US electricity generation. Yet the infrastructure is aging, with most reactors averaging around 40 years old.

Source: U.S. Nuclear Regulatory Commission

- Experts warn we should be cautious when it comes to revamping nuclear power when considering the issue of nuclear waste disposal and the potential for catastrophic disaster. Yet with proper maintenance and care, nuclear power can beat its rep and emerge as a safe and reliable energy source.

- Last week the Department of Energy awarded vouchers to 7 companies in order to accelerate the innovation and application of advanced nuclear technologies under the GAIN initiative. The vouchers do not offer direct financial awards, but rather provide funding to DoE laboratories to assist businesses overcome technological and commercialization hurdles.

- Alpha Tech Research Corps. is collaborating with Argonne National Laboratory in order to gather data to determine the size and design for a molten salt microreactor concept.

- General Atomics will work with Oak Ridge National Laboratory to help inform material behavior models required to license the use of silicon carbide structures in reactors.

- Ultra Energy will also work with Oak Ridge National Laboratory, but will focus on organizing and designing high temperature reactor testing and furthering the development of a prototype detector that is planned for commercialization.

- Westinghouse Electric Co. will work with PNNL and Idaho National Laboratory and focus on corrosion and hydrogen behavior in the cladding from two different coating processes.

How energy communities are utilizing the Inflation Reduction Act

- Last year’s Inflation Reduction Act, aimed at lowering the federal government’s budget deficit and upholding the Biden-Harris commitment to clean energy advancement via generous tax credits, is being put to action across the U.S.

- The landmark bill allocates nearly $370B toward repurposing old fossil fuel infrastructure and employing displaced workers, specifically in so-called “energy communities” (areas whose economies are dependent on fossil fuels) where an additional 10% tax credit is being offered.

- Minnesota, for instance, plans to invest its $3 million IRA grant toward a study regarding the impact of green initiatives in disadvantaged neighborhoods. MN has already done extensive work in the climate planning space with the state being on track to reduce their emissions 80% by 2050.

- New Hampshire, which has long lagged behind other New England states on climate action, incorporated its recently awarded federal tax credit into a $15.2B budget that allows the state’s Department of Environmental Services to create a new climate plan.

- To gain momentum, some initial investments are being made into hiring managers and gathering feedback from a wide range of stakeholders.

- The grant will provide NH with a much-needed push (as the state hasn’t produced an updated climate plan in nearly 15 years).

- In Northwestern Illinois, 175,000 metric tons of carbon dioxide (equivalent to the emissions of 38,000 vehicles) are being pumped out of Adkins Energy facility everyday.

- Due to the IRA’s uncapped tax credits, this facility and others like it are beginning to utilize carbon capture, that is, permanently storing emissions into the ground.

- While the IRA has undoubtedly jump started plans to combat climate change and reduce carbon emissions throughout the country, some critics argue the plan is too radical and the dent in GHG emissions will not be worth the cost. The Brookings Institute projects that the 45Q program alone will cost upwards of $100B, sounding alarm bells all throughout Washington.

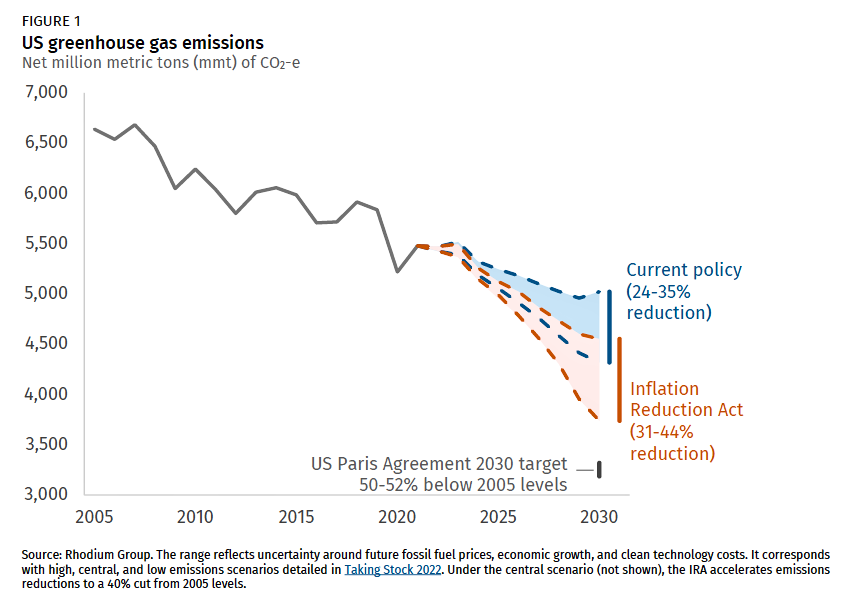

- Even so, passage of the IRA speaks to the Biden-Harris commitment to clean energy advancement (with GHG emissions expected to reduce 44% by 2030!)

Source: Rhodium Group

- This is comforting to many who agree that climate change is an imminent threat – and climate resilience a worthwhile investment.

Natural Gas Storage Data

Market Data

Market data disclaimer: Data provided in the "Market Data" section is for the newsletter recipient only, and should not be shared with outside parties.