Energy Markets Update

Weekly natural gas inventories

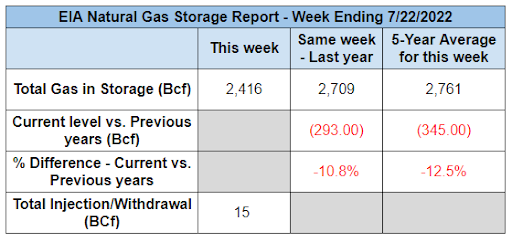

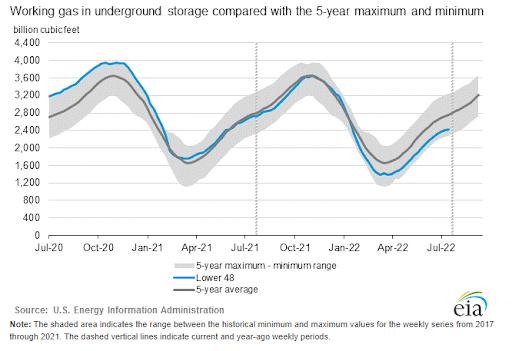

The U.S. Energy Information Administration reported last week that natural gas in storage increased by 15 Bcf. The five-year average injection for July is about 44.2 Bcf. Total U.S. natural gas in storage stood at 2,416 Bcf last week, 10.8% less than last year and 12.5% lower than the five-year average.

US power & gas update

- Nationwide heatwaves drive cooling demand, lift both short term and mid-term prices. Power demand up ~4 bcf/d from 2021.

- Balance of 2022 NYMEX gas futures are now closing in on the $9.26 peak established in the first week of June; we are back near the all-time highwater mark.

- Freeport LNG signals possible restart in September / October after the June fire that took the 2 bcf/d facility out of service.

- Gas storage injection numbers disappoint, dimming hopes for bearish downturn ahead of winter. Today's storage report was 10 bcf lower than expected and over 30 bcf lower than the July average.

- Most power markets now showing eye-popping winter 2022/2023 premiums for power and gas. We advise caution as premiums appear to be out of line with assumptions of even tight winter fundamentals.

Source: CME Group

Source: CME Group

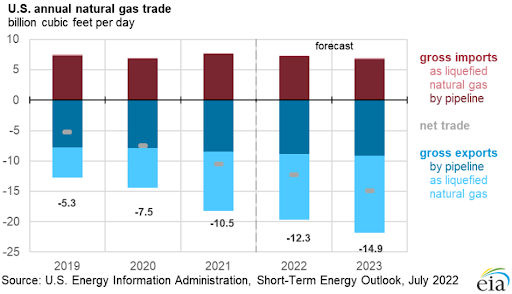

US now world’s largest exporter of LNG, but not to New England

- The US became the world leader in LNG exports during the first half of 2022, averaging 11.2 bcf/d of sendout, with a capacity of 13.9 bcf/d at its seven export terminals.

- Global demand and prices for the fuel have surged in response to the threat of curtailments to Europe by Russia’s Gazprom. Prices in Europe have ranged from $25-70 per MMBtu over the past year and currently hover around $45.

- Meanwhile, New England, the only region in the US that imports LNG, faces significant competition from Europe to land cargoes. The price for January 2023 pipeline gas into New England exceeded $45 per MMbtu in trading this past week.

- New England has been inching its way down the energy plank for years now due to its inability to build critical energy infrastructure or to collaborate effectively across state lines.

- It also suffers from senseless federal regulation that prohibits any foreign-built, foreign-owned or foreign-flagged vessel from engaging in coastwise trade within the United States, i.e., the Jones Act of 1920.

- This means that New England must import LNG from foreign suppliers. It is prohibited from taking lower cost gas from nearby US LNG terminals because the US does not have any domestic LNG vessels.

- Nonetheless, the convergence of the futures market for New England gas with the global LNG price, is a head scratcher. In January 2022, New England imported a little more than 2 bcf, or 1 LNG cargo representing < 2% of consumption for the month.

- Pipeline gas into New York for January 2023 trades at roughly $20/MMbtu compared to New England at $45, the spread predominantly attributed to presumed constraints to be rebalanced at the higher clearing price of imported LNG.

- In our view, the notion that 2% of the gas supply will contribute to a basis differential of $25 for the monthly contract, doesn't add up. We do however see high potential for daily spikes in the cost of gas during cold snaps, potentially testing $100 per MMbtu.

Massachusetts passes ‘landmark’ climate bill to decarbonize economy

- Last week the Massachusetts legislature passed a bill that would establish a minimum goal of 5.6 GW offshore wind generation under contract by 2027, incentivize electric cars, reform efficiency programs for low-income residences, and kickstart a program for municipalities to offer green home renovations, focusing on affordable and multi-family housing developments.

- The bill includes a dizzying array of targets and proclamations; the existing target of 4 GW by 2027 was made less than 18 months ago when the Baker Administration increased the initial 1.6 GW (already contracted) by 2.4GW.

- Energy usage reports will be required on an annual basis for buildings larger than 20,000 square feet, all part of efforts to reduce emissions to 50% of 1990 levels by 2030, and phase out sales of combustion engines by 2035.

- The bill had heavy support from state and national environmental groups and it now awaits the Governor’s signature. The real work begins when the Commonwealth's regulatory agencies (primarily DOER and DPU) digest it and turn it into actionable regulation.

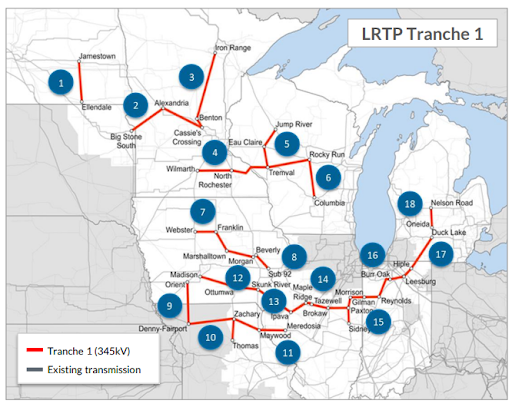

MISO approves historic $10.3B investment in transmission

- This past week, the Midcontinent ISO (MISO) approved $10.3 billion of long-range transmission plan (LRTP) projects to facilitate the transition to clean energy, the largest single portfolio of grid projects approved in the country.

- The 18 projects in the Midwest region of MISO makeup Tranche 1 of the LRTP projects, and are expected to introduce 53 GW of renewable generation onto the grid and lower carbon emissions by 63%.

- This initial Tranche of projects targeting northern MISO states, will also increase reliability and lower congestion costs. MISO anticipates over $37B in benefits related to the projects, a benefit cost ratio of 3.7 to 1.

- Tranche 2 projects are associated with the Midwest region as well, while Tranches 3 and 4 focus on MISO’s South region and link the two together. The total cost of these LRTP projects is expected to exceed $100 billion, however these projects will take some time to review.

- Many stakeholders, though excited about the approval of Tranche 1, are strongly urging MISO to approve the other tranches due to increasing demand for electricity along with frequency of extreme weather patterns.

- Although cost for these projects is significant, MISO gained approval from FERC to allocate the costs broadly by subregion (the Midwest in Tranche 1).

- All projects involved in Tranche 1 are expected to be operational by 2030 at the latest. They range in cost from $231 million for a segment in Iowa to $1.05 billion for a segment in Wisconsin.

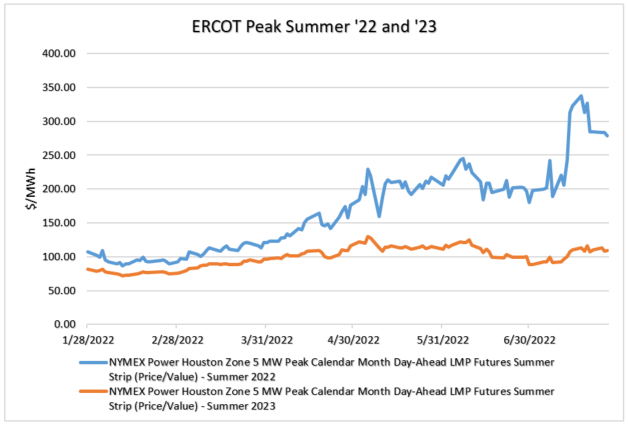

Texas sets 8 peak load records since June 12

- Eight peak load records have been set by ERCOT since June 12, as Texas has been enduring record temperatures since May.

- Maximum system load records were last set in August of 2019, and ERCOT is fighting to keep up with demand that they expect to further increase over the coming weeks.

- The grid has been lucky to keep up with demand; many coal plants are not performing well in the heat and temperatures have been extreme.

- Experts expect that the grid may exceed 80 GW of load at some point in the summer. The grid had neared 79 GW of peak load on July 12.

- Though ERCOT has made many attempts to improve grid reliability for the future, many of these revolve around reliability in the winter following the disastrous consequences of the winter storm in February 2021.

- High energy costs are expected to plague ERCOT for the foreseeable future. Real-time prices have skyrocketed, exceeding $5,000/MWh for a span of a few hours on July 13. Weekly futures contracts also rallied for the remainder of summer.

Natural Gas Storage Data

Market Data

Use the filters to sort by region

Market data disclaimer: Data provided in the "Market Data" section is for the newsletter recipient only, and should not be shared with outside parties.