Energy Markets Update

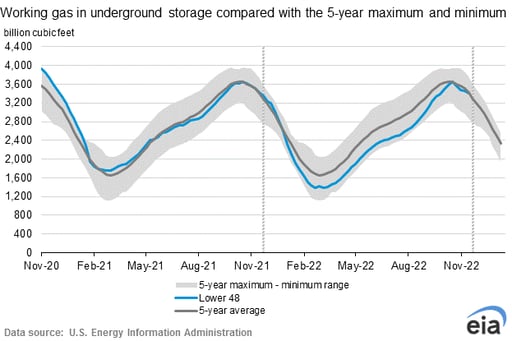

Weekly natural gas inventories

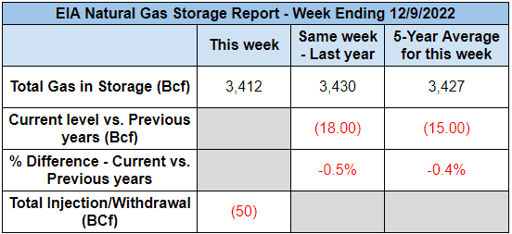

The U.S. Energy Information Administration reported last week that natural gas in storage decreased by 50 Bcf. The five-year average withdrawal for December is about 94 Bcf. Total U.S. natural gas in storage stood at 3,412 Bcf last week, 0.5% lower than last year and 0.4% lower than the five-year average.

US power & gas update - year in review

-

In our final newsletter of 2022, we reflect on what has been one of the most turbulent and challenging years for energy buyers in recent memory. Despite a highly uncertain winter ahead of us, the year is closing out in a relative downtrend. However virtually every gas and power market in the US has moved over 100% from peak to trough this year. NYMEX gas started off around $4 per MMBtu in January. By springtime, we blew past $9 and the market has struggled to find rangebound footing ever since. Meanwhile, we watched anxiously as European gas prices approached $100 per MMBtu this summer. We’ve seen Q1 2023 power in New England move from $100/MWh to $300/MWh this year. All of this has profound impacts on our customers and partners tasked with managing budgets and implementing hedging programs. The volatility in 2022 has made it clear that planning, proactiveness, and patience are essential to riding out the storm. We thank our colleagues, partners, and customers for their camaraderie and confidence.

Check out our recent webinar on how to manage through volatility: How to Manage Energy Budgets Through Volatility

Some highlights from the past two weeks:

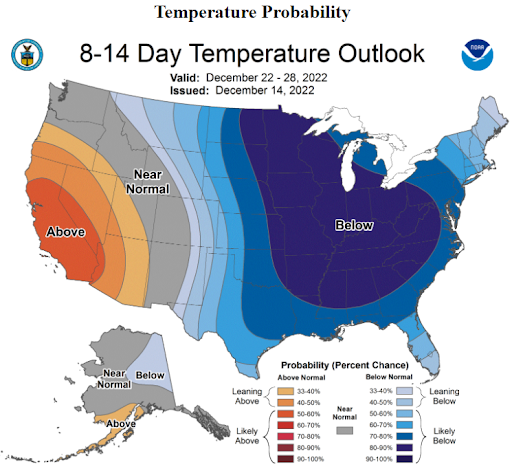

- Weather forecasts for the back half of December have shifted markedly cooler, adding support to the near term NYMEX contracts.

- We’ve seen gas futures for 2023 increase by about 20% over the past 10 days. The 2023 NYMEX strip is currently trading in the $5.25 per MMbtu range.

- This week's gas storage withdrawal of 50 bcf, and last week’s of just 21 bcf were quite a bit smaller than average for this time of year, indicating the more temperate weather thus far.

- Net gas demand has tapered some in the past 6 weeks as compared to YOY trending thus far in 2022. It’s difficult to deduce entirely how much of this is weather related vs some preliminary tapering of economic activity.

- Freeport LNG, the currently shuttered LNG export terminal, has provided guidance that it will resume operations in mid-December with gradual ramp-up back to full capacity by March. The December start date seems likely to slip however; this week FERC sent Freeport a laundry list of conditions it must meet before restarting the terminal. Many analysts are now anticipating a January partial restart.

- The decline in oil prices, now ~$80 bbl, has been somewhat a surprise and almost certainly related to tapering in demand, primarily in China where strict COVID lockdowns have suppressed demand by as much as 30%-40% according to some estimates.

Source: NOAA

New wintertime surcharge expected for ERCOT’s large commercial customers - Firm Fuel Supply Service (FFSS)

- The Public Utility Commission of Texas (PUCT) ordered ERCOT, in response to Winter Storm Uri in February 2021, to develop a “firm-fuel” product that would improve grid stability by procuring close to 3,000 MW of capacity from generation resources that primarily rely on fuel oil instead of natural gas.

- The $53 million dollars spent on the Firm Fuel Supply Service Resources (FFSSRs) auction will compensate generating resources that meet a higher resiliency standard equates to just under $0.50 per MWh of forecasted load from November through March.

Firm Fuel Supply Procurement Services

Source: ERCOT - Suppliers of retail power in Texas are still determining how to account for the additional cost of this new ancillary service. Large commercial customers will likely absorb these additional costs, which will be passed through as additional line items on invoices this winter.

- Large commercial clients should expect an additional charge on monthly invoices from November through March.

New York’s Plan to Tackle Ambitious Climate Goals With New Transmission Lines

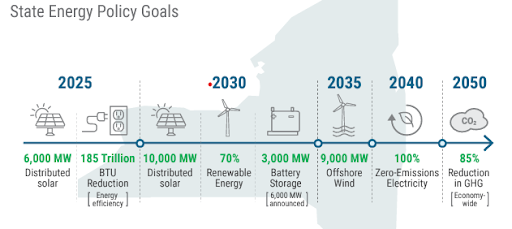

- In 2019 the state established the Climate Leadership and Community Protection Act (CLCPA), requiring New York to reduce economy-wide greenhouse gas emissions 40% by 2030 and no less than 85% by 2050 from 1990 levels.

- NYISO’s projected technologies and implementation schedule to reach these targets are provided below.

Source: NYISO - In the same year, New York City enacted Local Law 97 (LL97) as a key component of the larger set of laws known as the Climate Mobilization Act (CMA). LL97 established penalties for building owners that will be significant if the electricity generation mix does not improve through decarbonization in the coming years as the carbon limits provided for buildings ratchets down in 2030 and 2035.

- One challenge to achieving the CLCPA’s and CMA’s ambitious targets stems from the lack of downstate renewable generating assets and physical constraints.

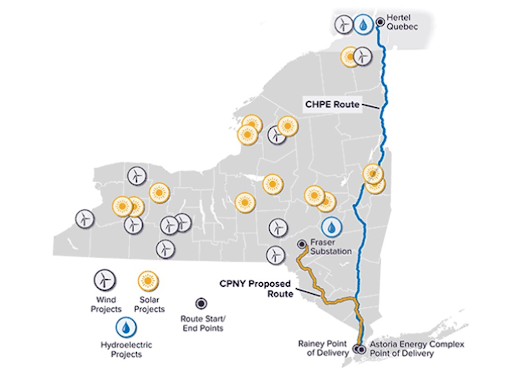

- The Champlain Hudson Power Express (CHPE) and Clean Path NY (CPNY) were selected to develop new transmission lines that deliver hydropower from Quebec and solar and wind power from upstate New York.

- The planned transmission lines are expected to provide 18 million MWhs of renewable energy to NYC each year, which would reduce greenhouse gas emissions by 77 million metric tons over the next 15 years, according to NYERSDA.

Source: NYISO

- The success of these projects is of high importance for the state and city to reach the carbon reduction targets of the CLCPA and CMA.

- Construction of CHPE began in November of this year. CPNY is expected to begin construction in 2024 and operation in 2027.

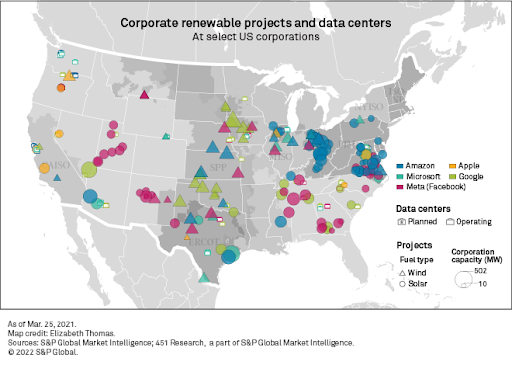

Tech Giants Prop up Renewables in 2022 Despite Headwinds

- The market for renewable energy credits is expected to double from $11.5 billion in 2021 to $26 billion in 2030.

- The Western Interconnect (Plains to CA) has dominated the market thus far, contributing to more than 40% of the overall market value. On the corporate side, the largest buyers by far have been big tech firms.

- Tech companies’ overall emissions have continued to increase despite heavy investment in renewable energy projects.

- Growing pressure from shareholders and federal tax benefits are likely to drive those investments in renewable PPAs significantly higher in the near future.

- According to data from the Clean Energy Buyers Association, Amazon.com Inc., Meta Platforms Inc.,Google LLC and Microsoft Corp. were the largest clean energy customers by announced megawatt volume from 2014 to 2021. Amazon has a goal to power its operations with 100% renewable energy by 2025. During the first four months of 2022 they announced 25 clean energy projects, equivalent to the same number of projects announced for all of 2021.

- Federal incentives such as the Inflation Reduction Act aim to further reduce the costs of solar panels, batteries and wind turbines primarily due to economies of scale as demand increases. In addition, the Inflation Reduction Act will allow for tax credits as high as 50% for projects utilitzing domestic-manufactured equipment. Credits can be claimed on projects that are completed during 2022 through the early 2030s.

Source: S&P Global Market Intelligence

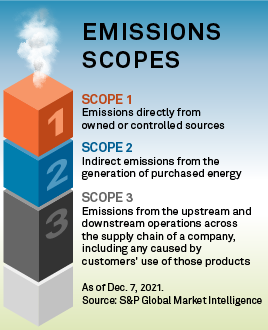

- Increasing pressure from stakeholders is focused on net zero Scope 1 through 3 (refer to image above). Companies can more easily tackle Scope 2 emissions by purchasing renewable power.

Source: S&P Global Market Intelligence - Tech companies including Amazon, have invested heavily in renewable energy projects that are close to their datacenters.

- PPAs have become more challenging to execute in 2022 due to interconnection delays, supply constraints, inflation, and concerns over a pending recession.

- In many regions, the strike price of a PPA has doubled in the past 18 months. Thus far, this does not appear to be slowing down the appetite of amongst the big firms.

Natural Gas Storage Data

Market Data

Use the filters to sort by region

Market data disclaimer: Data provided in the "Market Data" section is for the newsletter recipient only, and should not be shared with outside parties.