Energy Markets Update

Weekly natural gas inventories

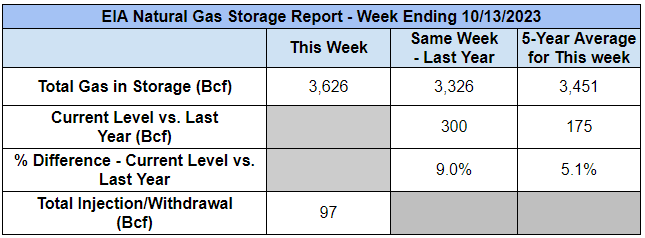

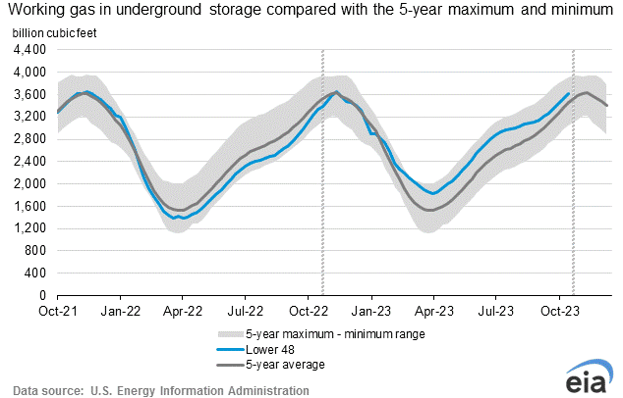

The U.S. Energy Information Administration reported last week that natural gas in storage increased by 86 Bcf. The five-year average injection for October is about 75.3 Bcf. Total U.S. natural gas in storage stood at 3,626 Bcf last week, 9.0% higher than last year and 5.1% higher than the five-year average.

Energy Market Update

- Thus far, the impact of the recent crisis in the Middle East has been mostly muted in the United States (see story below). Natural gas and power prices in the US showed no material change after the attacks in Israel. Global oil markets are inherently more prone to turmoil in the region, however they have mostly shrugged off the news. Oil prices are up about 2-3% since the attack but traders are cautious given the coinciding risks of an economic slowdown.

- The forward curve for US gas and power continues to show both meaningful and stubborn premiums beginning Q4 2024. This indicates some consensus around growing tightness in the market. Will it manifest? The answer most likely rests on weather and the production from the Permian basin, which some analysts have begun to question over the past year.

- After losing roughly 20% of natural gas drilling rigs across the US from January to August, the rig count appears to be stabilizing over the past 3 weeks, at around 120 rigs. This is dampening the most troubling concerns about the extent to which the market will become supply constrained next year.

- In its Short Term Outlook published last week, the EIA upped its Q4 dry gas production forecast by 1.8 Bcf/d to 114.32 Bcf/d, from one month earlier. The 2024 Q1 forecast was increased by about 0.43 Bcf/d. The EIA expects that storage inventories will top out at 3.85 tcf this fall, 6% above the 5-year average.

- The newest LNG terminal to enter service is expected to be Golden Pass in Texas. A recent FERC filing requested permission for commissioning and start up of Train 1 by November 20, 2023, far sooner than many analysts had expected. Golden Pass will eventually have 3 trains, each with a capacity of 0.8 bcf/d. Trains 1 and 2 should be operational in the second half of 2024.

- ExxonMobil's acquisition of Pioneer Natural Resources for nearly $60 billion emphasizes Big Oil's continued interest in US shale producers. It significantly boosts Exxon’s presence in the Permian Basin, the largest US oil-producing region. According to experts, this consolidation is driven by the need for economies of scale and cost reduction in a highly fragmented Permian shale market, where several major players including Chevron, Occidental, ConocoPhillips, and ExxonMobil are leading production.

- Corporate bond yields continue to climb as expectations set in that the Fed will remain steadfast in its quest to stamp out inflation. Bond yield spreads however, the premium that corporates pay above the risk free rate, have started to increase at tad in October, after declining from May through August. This is a possible indicator of increasing recessionary expectations.

- The renewable PPA market remains challenging for buyers, particularly in North American solar markets where costs are reportedly up 25-30% year over year. Buyers will need to get creative to find value in new projects next year.

- ERCOT has issued an RFP for 3 GW of either mothballed capacity or demand response for the upcoming winter. The Texas grid operator says it could be short if there is a repeat of the December 2022 winter storm Elliot.

Source: NOAA

War in the Middle East

- The war in Israel and Palestine is causing some uncertainty in regional markets but muted effects in the United States.

- Shortly after the initial conflict, European natural gas prices increased 14% since Israel is a major provider of natural gas in the region. Adding fuel to the fire were reports that Israel shut down a number of offshore natural gas facilities in Gaza’s missile range. This included the Tamar offshore field, which provides half of the gas supply to Israel and also supplies Egypt and Jordan.

- Israel will now have to get gas from elsewhere, which could drive up competition for natural gas in the market. The issues are mostly regional at the moment, but if fighting continues and expands to more of the region, it could become a global natural gas market issue.

- Oil markets are not as concerned at present, but if the war draws in Hezbollah in Lebanon and a larger presence from Iran, markets will likely rally. If it’s found that Iran unequivocally assisted Hamas, other countries could retaliate by imposing sanctions on Iranian oil. Iran has helped offset Saudi Arabia’s export cuts by adding more supply to the market, but increased sanctions could widen the supply/demand deficits we saw earlier in the year.

- Oil production in the US hit an all-time high for the week ending October 6 (13.2 million bbl/day). The US is finalizing a deal with Venezuela that would lift sanctions on the country's oil industry for a six month period. This would free up additional barrels while Venzuela prepares for national elections.

- All said, US energy prices should not be affected by this conflict as long as it does not expand to Iran or heavily affect European energy prices in the long term. If this does come to pass, the most prone regions would be New England for the upcoming winter strip.

NY PSC Rejects Renewable Energy Rate Hikes

- In a highly anticipated ruling last Thursday, October 12, the New York State Public Service Commission (PSC) rejected petitions submitted by Empire Offshore Wind LLC and Beacon Wind LLC, Sunrise Wind LLC, and the Alliance for Clean Energy New York, Inc. (ACENY) for extra consumer funding by offshore wind developers and a renewable energy association for offshore and land-based projects.

- The projects seeking higher payments were extensive: four offshore wind and 86 land-based renewable projects representing 25 percent of the forecast electricity demand in 2030.

- The decision by the PSC leaves developers to decide whether to cancel contracts with NYSERDA, sacrificing millions of dollars in security payments. It will almost certainly result in the termination of the 924 MW Sunrise Offshore Wind project contracted by Eversource and Orsted, but the cascade of dominoes could be many.

- In short, many developers entered into fixed price contracts with the state in recent years, but a runup in interest rates, supply chain, and labor issues have left many of them unable to profitably finance and complete these projects.

- Similar financial pressures led to the termination of some offshore wind power purchase agreements in the US, including Rhode Island Energy's pull-out from a project with Ørsted and Eversource. Massachusetts lost almost 2,000 MW of contracted offshore wind capacity this summer.

- The contracted NY projects are a central component to New York State’s plan to achieve its Climate Leadership and Community Protect Act Targets (reduced emissions by 40% from baseline emissions in 1990). However the PSC was clearly concerned about the precedent and rate impacts associated with agreeing to the rate increases. Granting the requested amendments would have resulted in up to 6.7% increases for residential customers and up to 10.5% for commercial or industrial customers on their monthly bills, based on service territory and the level of relief provided.

NYSEG Rate Case Update

- The New York Public Service Commission has approved a large three-year rate increase New York State Electric & Gas and Rochester Gas and Electric (parent Avangrid Utilities), along with billions of dollars of investments in reliability, resiliency and customer service.

- NYSEG serves more than 905,000 electricity customers and RG&E serves approximately 389,000 in the upstate region of New York.

- Regulators approved a levelized electric rate increase for NYSEG for the rate year beginning May 1, 2023 of $137.3 million, followed by $160.7 million for 2024 and $200.6 million for 2025. For RG&E, the increases are $50.9 million, $56.6 million and $65.3 million. Gas rates will increase as well.

- The approval includes $5.2 billion in total investments for the two utilities, including $1 billion “to focus on serving customers, with increased bill assistance and expanded protections during extreme temperature events.”

- Infrastructure investments include a circuit breaker replacement program, efforts to repair or replace transmission line infrastructure, a distribution load relief program to address power transformer capacity overload, substation rebuilds and more.

- The average NYSEG residential electric customer will see monthly bills rise more than 10% in the first year and more than 31% over three years. Average RG&E residential electric bills will rise 7.4% in the first year and more than 22% over three years.

Hydrogen Hub Funding Announcement

- Two years ago, the Bipartisan Infrastructure Law established the Regional Clean Hydrogen Hubs Program, offering up to $8 billion to support the development of hubs for clean hydrogen production, delivery, and use.

- On October 13th, the Biden administration announced the 7 hydrogen hubs that will split up to $7 billion of the fund. Specific sums to be awarded are still under negotiation.

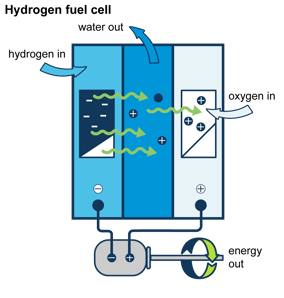

- Hydrogen power generation works by combining hydrogen and oxygen atoms. The hydrogen reacts with oxygen across an electrochemical cell to produce electricity, water, and small amounts of heat (US EIA). However it is important to note that hydrogen is not a source of energy. It is stored energy and it must be created using high amounts of energy inputs, preferably from renewables, but this is not a given.

Source: US EIA

- Benefits of the selected Hydrogen Hub projects :

- Job Creation. The selected hubs will create tens of thousands of jobs.

- Investment. The selected hubs will generate over $40 billion in investment and support domestic manufacturing.

- Union Labor. Several of the hubs were developed in partnership with unions, with three requiring project labor agreements (PLAs).

- Clean Sourcing. About two-thirds of total project funding is to be allocated to “green” (electrolysis based) production (creating hydrogen from non-emitting sources).

- Environmental Benefits. The seven selected hubs will eliminate 25 million metric tons of CO2 emissions from end uses each year.

- Community Engagement. The legislation includes provisions for Community Benefit Plans, ensuring all communities share in benefits, especially those historically overburdened by pollution.

- Downsides to of Selected Projects:

- The engineering challenges around hydrogen remain abundant. It is the smallest element, and it often requires highly specialized equipment to process, transport, store and combust it. There is a great deal to be learned from these early demonstration projects.

- Non-Green Hydrogen. Some of the projects source the energy required to isolate hydrogen from non-renewable, emitting sources.

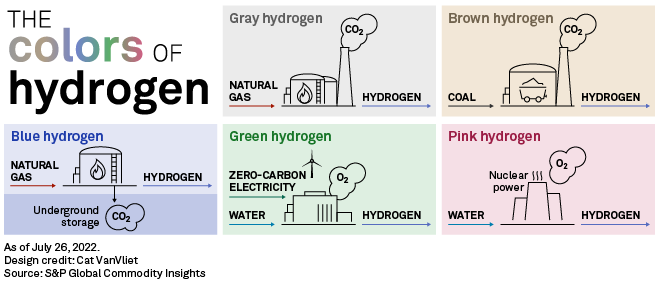

- The viability of hydrogen as a clean energy source is debated as certain methods of isolating hydrogen use emitting energy mixes to power themselves. Such methods align with the “gray”, “brown” and “blue” methods of hydrogen production below. “Pink” hydrogen is debated, too, as some debate how “renewable” and “non-emitting” nuclear power is.

Source: S&P

- When compared to battery storage for energy security, hydrogen may be more cost-effective at large scales, however this needs to be proven out. Additionally, hydrogen can be produced from a variety of sources, while batteries currently rely on scarce metals and hard-to-source lithium-ion. On the other hand, battery storage systems are more established, and lithium-ion is less volatile than stored hydrogen.

- Currently, most hydrogen energy is produced from emitting sources, which may give it a non-green reputation. However, investments like that from the Biden administration may be what is needed to boost the nascent industry and give it the opportunity to show its potential.

Carbon Accounting Requirements in CA

- Four weeks ago, we reported on California’s new emissions disclosure laws requiring companies with over $1 billion in annual revenue to report carbon emissions. On October 7th, California governor Gavin Newsom officially signed the legislation.

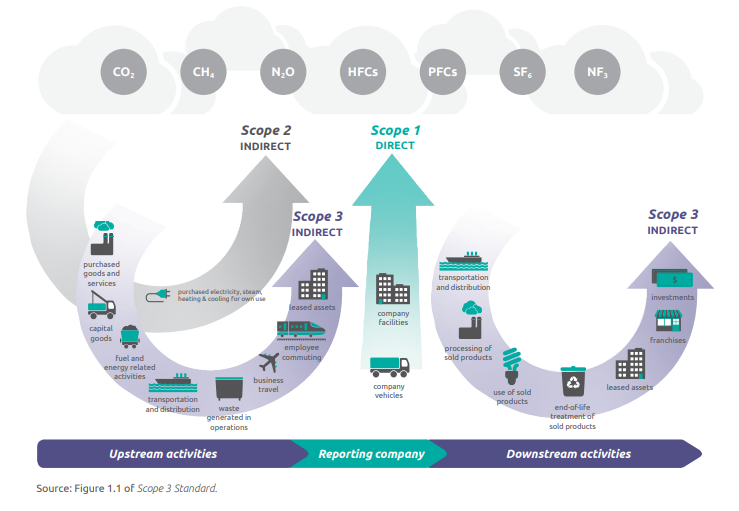

- The new legislation requires public and private entities doing business in California with more than $1 billion in revenue to report emissions falling under scopes 1, 2, and 3.

- The law requires that disclosures for scope 1 and 2 emissions are to begin in 2026, while the notoriously harder-to-track scope 3 emissions are to begin disclosures in 2027.

- Businesses could face penalties up to $500,000 per year for violations. Because tracking them is more complex, scope 3 reporting errors made with a “reasonable basis” and in “good faith” will not warrant penalties between 2027 and 2030.

- For reference, see definitions by scope below.

Source: GHG Protocol

Source: GHG Protocol

- Looking ahead, Newsom remarked that future revisions to the law are likely in future legislative sessions.

- The law also requires emissions figures to be certified by a verified third-party, such as Veolia. We aim to provide this service, along with advisory and support services, to clients newly subject to these reporting requirements.

- Veolia has corollary experience with public carbon reporting requirements through similar offerings on the east coast pursuant to regulations like BERDO in Boston and BEUDO in Cambridge, MA. We hope to be able to provide the same services to our clients subject to the new reporting requirements.

- Please reach out to commodity@veolia.com Veolia’s business development team for information on how to begin working with Veolia to report and certify these standards.

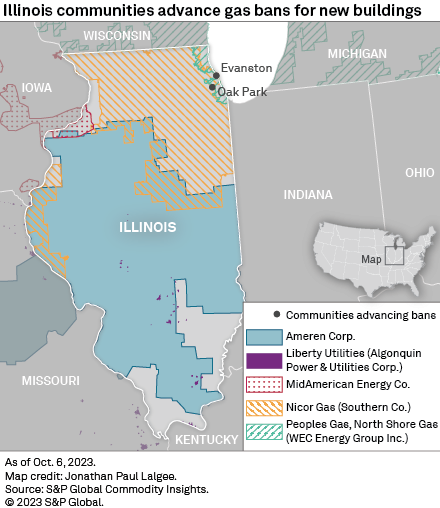

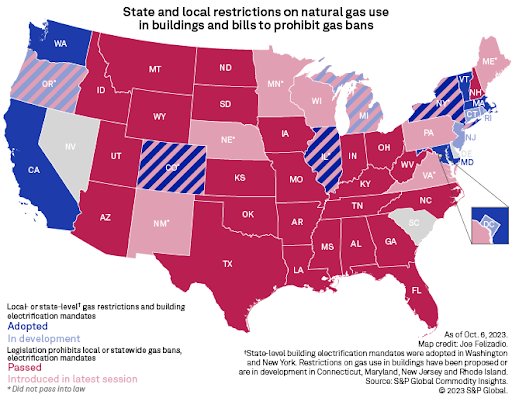

Gas Bans Arrive in the Midwest

- A national push to restrict natural gas use in buildings is gaining traction in the Midwest after remaining largely confined to the East and West coasts for several years.

- Gas bans gained a toehold in Cook County, Ill., the nation's second-most populous county, as Chicago-area policymakers look to building electrification to support their climate goals. The Board of Trustees in Oak Park, Ill., on June 20 adopted the Midwest's first local gas ban for new single-family homes, apartment complexes and other commercial buildings. The board unanimously supported the provisions, included as amendments to 2021 model building codes for residential and commercial construction. The codes required electric-powered air-source or ground-source heat pumps for space and water heating, as well as electric vehicle charging infrastructure. They allowed fossil fuel use for emergency backup in all building types and for commercial kitchens in mixed-use construction.

Source: S&P

- While Oak Park and Evanston opted to develop local ordinances restricting gas use in buildings, all Illinois communities could soon have a pathway to mandating all-electric construction and retrofits. State code officials are developing stretch energy codes for residential and commercial buildings, which will give communities the option to adopt more stringent building energy standards than the base code requires. The draft stretch codes include appendices that communities can adopt to require all-electric new construction. The Illinois Capital Development Board will finalize the stretch energy codes by Dec. 31, 2023, and make them available for adoption by June 30, 2024.

- Policymakers in Ann Arbor, MI have pivoted from pursuing a gas ban in new buildings to overhauling how the city heats its homes and workplaces. The city is exploring options to replace gas distribution with a lower-emissions method of heating buildings by renegotiating its gas franchise, currently held by DTE Energy Co. subsidiary DTE Gas Co. Local leaders determined that combusting gas for heating, cooking and other end uses is not consistent with the city's goal of achieving community-wide carbon neutrality by 2030.

- Five states passed laws to protect access to gas utility service in 2023, and gas ban opponents were looking to eke out another win before year-end in Wisconsin. Gov. Evers on Aug. 4 vetoed Wisconsin Senate Bill 49, which would prevent the state or local governments from restricting access to utility service based on the type of energy supplied. Republicans used their supermajority in the state Senate to override Evers' veto in a strict party-line vote in September, but the bill still needs support from two-thirds of the state Assembly to pass into law.

Source: S&P

Natural Gas Storage Data

Market Data

Market data disclaimer: Data provided in the "Market Data" section is for the newsletter recipient only, and should not be shared with outside parties.