Energy Markets Update

Editor’s Note: Rising utility costs have become a hot topic at both the conference table and the kitchen table over the past year. The issue highlights a conflict between the desire for affordable energy and the hard reality of how markets and power grids actually work. Wholesale commodity markets, driven by fluctuating natural gas prices and extreme weather, were the primary culprit in the most recent round of sticker shock last month. Those impacts will linger for at least another month or two. However, the broader impacts of capacity shortages in PJM and MISO, and various ancillary programs in NEISO will be much longer lived.

It’s time to review the basic components of a kWh and then work to dissect this complex landscape, analyzing why a ratepayer in California pays nearly triple the per-kWh rate of one in Louisiana, and then highlighting other trends that influence why costs shift and what you can do about it as a consumer. From capacity market reforms to contentious rate cases, there are many moving pieces we’re following in 2026.

Table of Contents

-

Echoes of 2025: Navigating This Year's Rate Case Environment

-

The Future of PJM Capacity: Proposed Market Reforms and Implications

Weekly Natural Gas Inventories

Source: EIA, Veolia

Energy Market Update

- Gas and power markets kicked off 2026 with a whirlwind. Winter storm Fern led to surging prices nationwide, and markets braced yet again this week as a Nor’easter returned blizzard conditions to the East Coast.

- Although the latest storm delivered >3 ft of snow in some parts of New England, markets have not responded with the same level of panic-driven price premiums observed during Fern. The storm was smaller in size and duration, while temperatures were more moderate. On Tuesday (2/24), spot power prices in New England hit $91/MWh, while prices surpassed $630/MWh during Fern.

- The March NYMEX contract settled at $2.969/Dth yesterday, staggeringly below February’s 3-year high of $7.46/Dth. The NYMEX strip for the balance of 2026 sits at $3.39/Dth, down 2% week-over-week and 19% compared to this time last month. The ‘27 and ‘28 strips remained mostly flat.

- Forward power prices are trading below trailing 12-month settled prices in key hubs like NYC and Boston. The discount is largely driven by the Nov-Jan strip for 2027/28, which continues to trade well below this winter’s prices driven by Fern, though our historical analysis suggests there is still a bit of premium built into next winter’s strip.

Source: S&P, Argus

- Before this week’s Nor’easter, February was comparatively mild as the market rebalanced and reverted to “pre-Fern” trends. This was after a record three-week 851 Bcf storage withdrawal that surpassed the 2017–18 winter record.

- This week’s EIA storage report showed a mild withdrawal of 52 Bcf, trimming the deficit to just 7 Bcf below the 5-year average.

- End-of-winter storage estimates have dropped 10% since the start of ‘26, leaving less buffer against late-season cold snaps. Storage is now projected to end near 1.698 Tcf - similar to last winter but concerningly lower for the risk-adverse buyer…

- The outlook for the remainder of the winter looks stable but weather dependent; mild weather and continued strong production should keep prices flat, but any unexpected late-winter cold could rapidly bring back volatility. NOAA's short-term forecast supports a bearish outlook, though given the nature of this winter season, we remain vigilant.

Source: NOAA

Other Stories We're Tracking Around the Country and Industry:

- EPA's withdrawal of the 2009 GHG endangerment finding earlier this month (2/12) is likely to create new regulatory uncertainty across the US energy sector, exposing companies to a potential new wave of state-level climate lawsuits, in the absence of a Federal emissions control mandate.

- Our colleagues at Veolia’s Flexible Solutions group published their analysis of Phase 2 of New Jersey’s statewide energy storage incentive framework, the Garden State Energy Storage Program. New Jersey readers will find these Phase 2 launch updates particularly interesting.

- President Trump has moved to extend FERC Commissioner LaCerte's term to 2031. First appointed in July 2025 to replace a departing Democrat, LaCerte’s renomination solidifies the commission's makeup as it faces urgent decisions on new generation and transmission infrastructure.

- On February 12, the New York PSC approved NYSERDA’s Offshore Wind Implementation Plan, adopting a “pay-as-you-go” funding model for LSEs and allowing OREC sales through long-term contracts to help reduce overall cost obligations.

- Symmetry Energy Solutions has been acquired by NextEra Energy Resources. According to NextEra, day-to-day operations remain unchanged with no disruption to existing service or contracts for Symmetry’s 5,000+ large C&I accounts.

- Energy managers can breathe a sigh of relief as Congress has secured $33 million in annual funding for the ENERGY STAR® program through 2026. This decision protects essential, no-cost benchmarking tools like Portfolio Manager®, which are vital for tracking building performance and complying with local and state regulations.

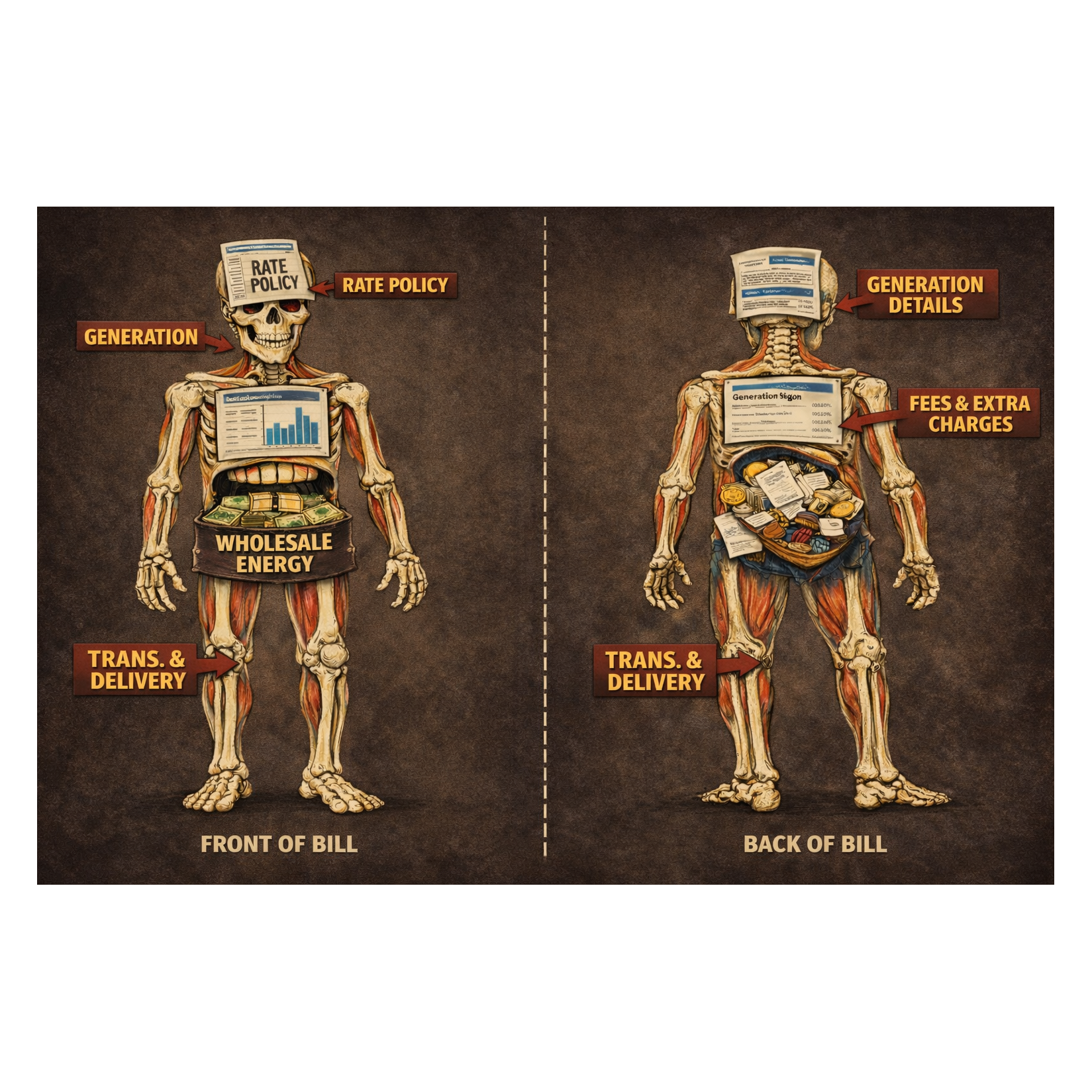

Anatomy of a Utility Bill: Diagnosing Regional Rate Shock

Understanding your electricity bill has never been more critical. While the national average retail rate rose about 4¢/kWh from 2020-2025, some regions saw increases three times higher, highlighting stark geographic differences. This article examines how supply costs (generation and commodity) and delivery costs (transmission and distribution) combine differently across major U.S. markets. In the Northeast, rising wholesale and capacity prices drove supply-side volatility; in California, delivery-side costs such as wildfire mitigation and grid hardening led the surge. Most of these increases are pass-through operating costs and the increases have not meaningfully enhanced utility earnings. Without improved earnings, utilities lack capital for the infrastructure investments that could address the root causes of these rising costs.

When you open your electricity bill, you're looking at the end result of a complex chain of costs that vary dramatically by region and market structure. At its core, your electricity bill consists of two major components:

1. Supply Costs (Commodity): The cost of generating or purchasing the electricity itself. This cost includes various components such as energy, capacity, renewable portfolio standard charges and cost-to-serve charges.

2. Delivery Costs (Transmission & Distribution): The cost of maintaining poles, transformers, wires, and infrastructure to deliver power to your home. This includes various components such as distribution, transmission and other miscellaneous charges.

The article below includes stack charts for several major markets that illustrate the key retail rate components paid by end-use commercial customers in 2025.

The relative impact of these components varies dramatically by region and market structure. In deregulated electricity markets (PJM, ISO-NE, CAISO, etc.), where utilities don't own generation assets, supply costs are directly tied to wholesale market prices. In traditional vertically-integrated markets (ie: Pacific Northwest, Mountain West, and Southeast US), utilities own their generation and recover costs through regulated rates.

Based on a recent analysis done by CRA, national average electricity retail rates from the 2020-2025 period for primarily residential customers have remained relatively stable, increasing only by 4¢/kWh, while a subset of states have experienced increases three times larger, driven primarily by their respective operational factors, as depicted in the graphic below.

Source: CRA - Retail Rate Trends in the US

Source: CRA - Retail Rate Trends in the US

The various factors impacting these larger rate increases in markets, such as the Northeast and CAISO, are covered in the section below.

The Northeast: A Case Study in Wholesale Market Exposure

The Northeast region, particularly states within ISO New England and PJM, has experienced the most dramatic supply-side-driven rate increases. For example: Since 2020, retail rates in Massachusetts have increased by up to 8.4 ¢/kWh, however due to the volatility of supply costs as compared to delivery costs, that change has been both positive and negative year-over-year .

The primary culprit is surging wholesale electricity market prices. In deregulated markets like ISONE, NYISO, and PJM, utilities that don't own generation must purchase power from wholesale markets. When wholesale prices spike, these costs flow directly through to retail customers, increasing the costs for energy, capacity, and ancillary services (A/S), etc. as shown in the chart below. Source: Veolia

Source: Veolia

PJM Interconnection: Capacity Market Pressures

In the PJM region, supply-side costs have been driven by factors beyond energy prices. The capacity market, which ensures adequate generation resources are available to meet future demand, has added high costs:

- PJM's capacity market prices increased substantially by 833% between the 2024/25 and 2025/26 delivery years, particularly in constrained areas

- A surge in projected demand from data centers, combined with delays and high costs for building new power plants, and PJM’s market structure, caused capacity prices to skyrocket

- Recent agreements among PJM state leaders and federal officials aim to cap prices, accelerate new generation development, and ensure data centers pay for the capacity built to serve them

Source: Veolia

California: A Delivery-Side Story

California (CAISO) has also experienced rate increases of 12¢/kWh over the last five years driven by factors beyond wholesale market volatility. The rate increases stem primarily from delivery-side (ie: distribution) costs rather than supply-side volatility, demonstrating how regional factors create vastly different bill impacts. Some of the factors that contributed to the delivery-side cost increases are: wildfire mitigation investments and state’s rooftop solar compensation structure.

Source: Veolia

Understanding the anatomy of your bill and the factors driving each component is essential to anticipating future cost trends. Recent increases largely reflect supply- and delivery-side volatility and consist primarily of operational expenses recovered on a pass-through basis, without adding to utility earnings. Without improved earnings, utilities lack capital for the infrastructure investments that could address the root causes of these rising costs. In effect, these rate increases cover only immediate operational costs without funding the capital investments needed to address the underlying “principal” of rising electricity cost pressures.

Given these dynamics, the affordability solutions must be region-specific. Policymakers should focus on the distinct cost drivers within their jurisdictions rather than applying broad national remedies, ensuring that strategies target the underlying sources of rate pressure rather than the symptoms.

DASI's Dilemma: Reliability at What Cost?

A recent shift in New England's energy market, designed to bolster grid reliability, has had an unexpected side effect: unprecedented cost volatility. Ancillary service charges, once a minor line item, have soared far beyond projections, and these costs are now appearing on consumer bills—even for those with fixed-price contracts. Our latest analysis unpacks the billion-dollar consequences of the new Day-Ahead Ancillary Services Initiative (DASI) and explores the urgent fixes being proposed to restore stability.

-

Effective March 1, 2025, ISO New England launched the Day-Ahead Ancillary Services Initiative (DASI), overhauling how the grid procures essential reliability services. Replacing the Forward Reserve Market, DASI now prices and procures Flexible Response Services (FRS) and Energy Imbalance Reserves (EIR) 1 day in advance - elevating resource flexibility to a premium product. This shift aims to modernize the grid and enhance reliability by financially rewarding power generators for greater flexibility and responsiveness to real-time system needs. We previously covered DASI in an earlier newsletter.

-

Ancillary services are critical for maintaining grid stability, balancing supply and demand, stabilizing frequency, and ensuring reserves during disruptions. Under the previous system, these services were purchased months ahead at flat rates. DASI’s day-ahead procurement better aligns supply with actual grid conditions, especially as intermittent renewable energy. While it improves operational accuracy and incentivizes flexibility, it makes costs highly sensitive to daily market fluctuations like natural gas prices, generator outages, and extreme weather. This new approach has led to an unintended consequence: a dramatic and volatile increase in costs.

-

Ancillary services have historically been a small share of wholesale electricity costs, but DASI has driven expenses far beyond expectations. ISO-NE initially projected $135 million annually, but by January 2026, program’s cumulative costs reached approximately $1.15 billion. The chart below shows the weekly cost for various DASI components (excluding the “Closeout Charge Dollars” component) and cumulative cost since its inception.

Source: ISO-NE, Veolia

-

The weekly DASI rates have swung dramatically from $0.56/MWh to $122/MWh, compared with historical costs near $1.50/MWh, and closely track day-ahead LMP price volatility as shown in the chart below. Events like Winter Storm Fern had amplified effects where the settled monthly January rate was ~$40/mWh, significantly higher than any prior monthly rates.

Source: ISO-NE, Veolia

-

The financial impact of these escalating DASI costs is now being felt by retail energy consumers. Most electricity supply contracts allow these ancillary charges to be passed through, leading to higher, unpredictable bills. Even customers with fixed-price agreements are not immune, as suppliers use "Change in Law" provisions and other adjustments to recoup these unforeseen expenses.

-

In response to the significant financial burden on consumers, the grid's Internal Market Monitor has proposed three urgent adjustments to the DASI market. These adjustments aim to lower costs while maintaining reliability and improving market efficiency.

- Upward adjustment to the Strike Price: Increase the strike price to better match the short-run marginal costs of the resources, thereby reducing closeout risk, improving participation, and lowering reserve offer prices.

- Downward adjustment to the Forecast Energy Requirement (FER): Lower the energy requirement to account for the expected contribution from renewable generation, aligning procurement with actual system conditions, reducing the “energy gap”, and helping to put downward pressure on prices.

- Review of the Non-Performance Factor (NPF): Re-evaluate and potentially reduce the non-performance factor applied to operating reserve requirements, given improved performance incentives and outcomes. This will help lower NPF, thereby safely reducing the total volume of expensive reserves the system is required to buy.

-

While a final decision from ISO-NE on moderating DASI costs is expected before year-end, market volatility will persist. Veolia stands ready to navigate these changes, arming you with market insights, contract guidance, and proactive risk strategies needed to stay informed, prepared, and protected.

Echoes of 2025: Navigating This Year's Rate Case Environment

- While the flow of new rate case filings has been remarkably consistent over the last four years, the real shock is the sheer magnitude of the costs being requested. Currently, there are 91 open cases across 64 U.S. utilities (57% electric, 41% gas), but the eye-popping story is that the unprecedented dollar amounts at stake go back a year further (see chart below).

- Last year set a record with utilities requesting an unprecedented ~$22 billion in rate hikes - the highest annual total since S&P began tracking in their RRA reports (RRA). While rate increases were felt across the nation (see map below), Florida Power & Light and Consolidated Edison of New York led the pack with the largest requests. While regulators approved $11.6 billion of that total, it's crucial to note that some 2025 cases remain unsettled, carrying additional financial implications into this year.

- More to the point, the cases proposed before the Public Regulatory boards now total ~$14.5 billion in increases from cases filed in late 2025 and early 2026. Below we’ve charted some of the latest cases to be filed using data compiled from S&P RRA.

Source: RRA, Veolia - The largest rate case filed this year, so far, comes from Duke Energy Carolinas, raising questions about the promises made in their proposed merger. As we covered in “Duking it out in the Carolinas” last September, the utility claimed the consolidation would benefit customers - a claim that may now be contrasted by this significant rate hike request.

- In response to affordability concerns, politicians are intervening or posturing to address them. In New York, Governor Hochul is pushing for utilities to submit a "bare minimum" cost option in future rate filings. Similarly, Massachusetts' Governor Healey is urging regulators to scrutinize every line item to lower costs and bill volatility, a strategy that has proven successful in the past. This pressure comes as cases like National Grid’s current request for a $342 million increase are under review (RRA S&P Global).

- Understanding the timing and structure of these rate changes is crucial. Our analysts continually track these cases to help clients forecast the magnitude of unavoidable cost increases and, more importantly, identify strategic opportunities arising from changes in rate design, such as a shift toward demand-based rates.

The Future of PJM Capacity: Proposed Market Reforms and Implications

In a previous newsletter we covered the record-setting PJM capacity auction and subsequent FERC order requiring new rules for data center interconnection. This past month, federal and state representatives have directed PJM to take immediate action to address consistent capacity shortfalls that are negatively impacting ratepayers. Members of the National Energy Dominance Council (NEDC) and governors in PJM issued a statement outlining the tariff changes PJM must implement to properly manage large-load interconnection. A day later, the PJM Board issued its own letter outlining similar demands. Here are the key takeaways:

- The PJM Board filed for an extension of the current price collar ($175/MW-day floor and $325/MW-day ceiling) for the 2028/29 and 2029/30 Base Residual Auctions (BRAs). This mechanism protects ratepayers from capacity price increases by capping the maximum possible PJM auction clearing price. The motion is currently being reviewed by FERC.

- After a third straight year of capacity deficiency, PJM will file for a backstop capacity auction, in addition to its annual auctions, to procure new long-term generation resources. They will deliberate on providing 15-year price certainty for new capacity resources. Stakeholders support assigning a large portion of the cost of this auction to load-serving entities that refuse to bring their own capacity or be curtailable.

- According to the statements, PJM must improve its load forecasting methodologies. To be included in the forecast, large loads will need to formally prove their intent to interconnect and verify the required demand.

- PJM will be required to accelerate interconnection for new generation that passes the capacity backstop and large loads that bring their own generation. They must also develop a framework directing certain large loads to curtail usage during peak demand periods.

- See below the proposed timeline for the PJM capacity market overhaul.

Source: Latham&Watkins, Veolia

-

If the current BRA price collar is extended as planned, it all but guarantees capacity prices above $300/MW-day through 2030. Until further notice, ratepayers in PJM will feel the cost impacts of a grid that’s straining to keep up with capacity demands. If you’re looking for a silver lining, PJM’s price collar mechanism has helped reduce capacity costs by over $13 billion over the past three years. The 2027/28 auction would have cleared at over $500/MW-day without it, according to PJM, with subsequent years likely to follow suit. See the chart below outlining the historical clearing prices and projections for the next two years.

Source: PJM, Veolia

-

Extending the price collar is just the first step in what will prove to be a pivotal year for PJM’s capacity market. The bigger picture is that an overhaul of this market has become increasingly necessary as an unprecedented number of large loads interconnect to the grid. The proposed solutions are more dynamic, allowing large loads that generate their own power to jump to the front of the queue, while establishing strict rules for curtailing loads that don’t generate their own power. There are several remaining uncertainties, but the blueprint given to PJM shows some promise of shoring up capacity while simultaneously protecting ratepayers. We’ll be watching closely to see how this story develops.

Market Data

Market data disclaimer: Data provided in the "Market Data" section is for the newsletter recipient only, and should not be shared with outside parties.